You’ve probably heard of student loan forgiveness and the Public Service Loan Forgiveness program if you’ve read this site. You’re less likely to have heard of something called the FIRE movement. It stands for “Financial Independence, Retire Early.” Check out this knowledge bomb: you could potentially get student loan forgiveness after 10 years and retire using the PSLF program. If you’re planning on 20-25 year PAYE or REPAYE forgiveness, the math is still possible but a bit tougher.

We’ll focus first on how folks pursuing PSLF could utilize the program and a high savings rate to retire early. At the end, I’ll add in what you need to do if you’re pursuing a “tax bomb forgiveness” approach.

Suze Orman and others have thrown a lot of cold water on the FIRE movement lately. Falling stock prices, fears of recession, and a massive number of FIRE blogs with 27-year-olds claiming to be retired have brought out the naysayers.

Full disclosure: I tried to retire at the age of 25 after three years as a bond trader. I even wrote a book about the experience. I started Student Loan Planner® partly because traveling all the time and not being a good steward of my time weighed on me. The other reason was my prospective father in law telling me to get a job or proof of income to marry his daughter.

I don’t want you to necessarily retire in 10 years if you love your job. I simply want you to be able to retire if you chose to. When you keep working anyway when you could afford to retire and not work anymore, that’s called financial independence.

When you’re financially independent, you can tell your hospital system that you refuse to take night shifts or weekend call anymore. You could quit your job as a state prosecutor to run an ice cream shop. Maybe you’d even practice as a pharmacist part-time while spending more time watching your kids grow up. The options are endless.

For me, I was able to break free from a corporate existence that bored me. Now I set my own hours, work where I choose to and have a lot more job satisfaction because I feel like I’m making a difference. I want the same feeling for you.

We’ll focus on showing you the math behind this aggressive approach of getting your student loans forgiven after 10 years while also being free from required work at the same time.

First step: work for a qualifying employer and save over half your pay

To receive tax-free loan forgiveness under the PSLF program, you’ll need to work for a government or 501c3 non-profit employer full time for 10 years while making payments under IBR, PAYE, or REPAYE.

The reason why PSLF helps with early retirement if you have student loans over $50,000 is the limited repayment term combined with tax-free forgiveness.

With PAYE in the private sector, you’d pay for twice as long and would owe taxes on the forgiven balance. Not so if you use PAYE in the public sector.

That means your assets can truly be set aside for goals like financial freedom instead of getting rid of debt.

To get student loan forgiveness after 10 years, you also need to file employment certification forms (ECFs) annually with FedLoan Servicing.

Let’s assume that you figure out PSLF on your own or use a group like us to figure it out for you.

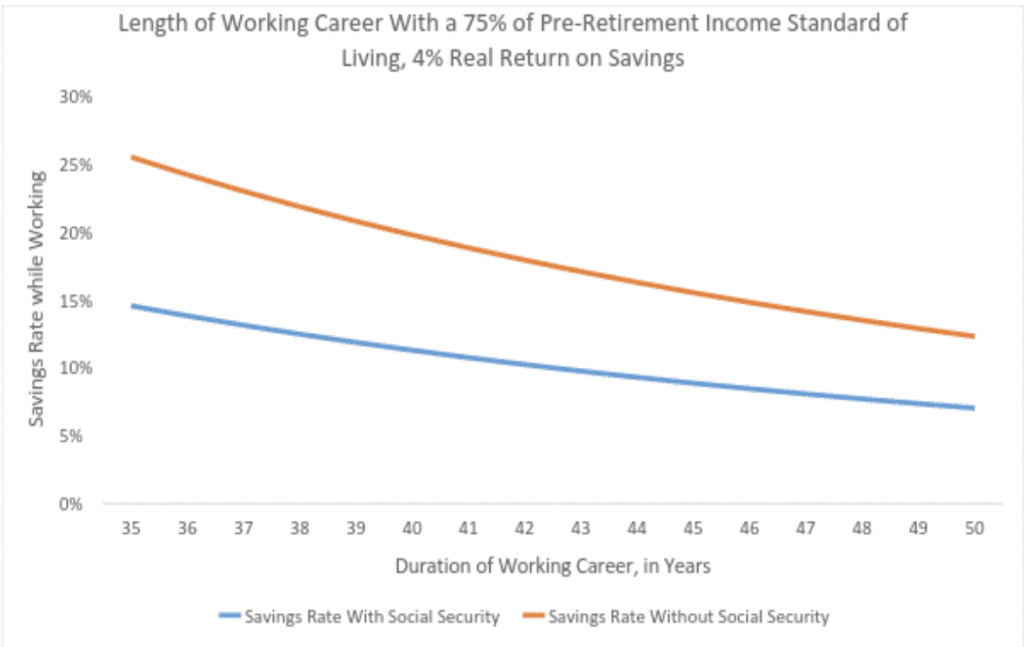

You’ll need to have a very high savings rate to achieve financial independence.

Consider this analysis I did for my book Mastering Your Money.

It shows how much you’d need to save as a percentage of your pretax income to retire and live on 25% of your salary.

Hence, if you earned $80,000 and wanted to retire on $20,000 per year, you’d need to save $40,000 per year (~50% savings rate) while earning an after-inflation return of 4%.

Here’s the hypothetical growth of your investments over time. I assume you could spend 4% of your portfolio every year forever while having the portfolio grow at the rate of inflation long term.

Year | Portfolio | Potential Income |

Year 1 | $40,000 | $1,600 |

Year 2 | $82,800 | $3,312 |

Year 3 | $128,596 | $5,144 |

Year 4 | $177,598 | $7,104 |

Year 5 | $230,030 | $9,201 |

Year 6 | $286,132 | $11,445 |

Year 7 | $346,161 | $13,846 |

Year 8 | $410,392 | $16,416 |

Year 9 | $479,120 | $19,165 |

Year 10 | $552,658 | $22,106 |

I can sense you might already be turned off by the idea that anybody could live on $20,000 per year.

Plenty of people do in the FIRE community. This level of lifestyle is called LeanFIRE.

At this level of spending, you’re clipping coupons, reading $1 per meal checklists on Pinterest, using Republic Wireless for your phone bill, driving a $2,000 Honda Civic and house hacking.

That said, the only way to save the amount we’re talking about is to live that lifestyle while working anyway. Hence, you’d just be continuing the same lifestyle that got you to financial independence in the first place. However, you wouldn’t have to work anymore unless you wanted to.

Second step: automate your investment plan with high contributions

If you put the high savings into your bank account, this strategy of retiring radically early fails.

Key in the approach is earning at least an above-inflation level return. One way to invest is with index funds such as VTSAX, the Vanguard Total Stock Market Index Fund.

As I write this article, that fund earned 6.61% annualized since inception in 2000. It might earn less than that going forward. Heck, it could even crash, but long term it’s likely to go up averaged out over time.

This VTSAX fund at Vanguard only costs 0.04% a year in fees. In contrast, a typical actively managed mutual fund sold by your neighborhood financial advisor might cost over 1% per year, or 25 times as much.

If you want to retire within only 10 years and are under 40, you’re not going to find many financial advisors that will get you there.

That means you need to take charge of your own finances.

One path to investing that $40,000 per year could look like this.

$40,000 a year = $3,333 per month.

You could split that equally between Vanguard’s Total Stock and Total International Stock Index Funds. You might add some bonds to the portfolio as well, perhaps 10% to 40% of the total portfolio.

If you want to figure out your own investment allocation, you can easily do that by using a site like bogleheads.org or reading a book like The Simple Path to Wealth.

If you’d rather have your investments managed in a low cost, intelligent way, you can use Betterment for only 0.25% per year. They have a modern digital interface that’s easy to use and understand. If you use the referral link in this paragraph, you get a month to year free.

Anyone with a steady job who wants to build wealth over time should be automating their investment contributions. For example, we set up a recurring monthly transfer from our bank account to four different Vanguard mutual funds and it took me 5 minutes.

This guarantees that no matter what’s going on in the economy, as long as we keep our jobs, we will be dollar cost averaging and growing our wealth.

Third step: maximize retirement accounts and your HSA for max forgiveness and financial independence

You might ask how the heck anyone could save $40,000 per year with $80,000 of pretax income when there are things called taxes and loan payments.

I won’t recreate the amazing guides that exist on how to get access to retirement funds early, even though you can use your money before 60 if you know what you’re doing.

To save a lot, you must know things like what tax bracket you’re in, what retirement accounts you have available, and how much you could contribute to all of them.

For example, the HSA limit for a family is $7,000 in 2019 and $3,500 for an individual. That money comes out tax-free. The new 401k and 403b limit for 2019 is $19,000.

Imagine the $80,000 per year income earner has a stay at home spouse and 2 kids. She could also make a spousal IRA contribution of $6,000 in 2019 and deduct it.

That means $19,000 (403b) + $6,000 (spousal IRA) + $7,000 (HSA) = $32,000. That’s the amount of tax-free money she could put away for her family.

Simulations I ran for this family would mean less than $10,000 total would go to federal income and payroll taxes.

Hence, the family could live on $30,000, put $8,000 into a non-retirement account, and meet these savings goals while paying all the appropriate taxes.

What about her student loan payments?

With an AGI of $48,000 and a family size of 4, this woman’s student loan payment would be $96 a month. That’s very affordable.

Could they get access to all the retirement money in 10 years after PSLF happens? That would prove challenging but not impossible. I didn’t spend a ton of time talking about hacks they could use. If you really want to go down the rabbit hole, google search “Roth IRA conversion ladder.”

I simply want to show it’s possible even if it’s not probable to expand your thinking.

Fourth Step: embrace frugality and living intentionally

You’ll never be able to reach financial independence and “screw you” money if you don’t have an unusually large savings rate.

Of course, you’ll never hit a high savings rate unless you have an intentional plan for your money.

Back in my early 20s, I was an extreme cheapskate. Why buy drinks at the bar when you could buy your booze at the grocery store and drink it before going out?

Why rent a one bedroom when you could room with four other single guys and spend 80% less on housing?

I was a bit of a weirdo.

Luckily, my wife rescued me and I’m now a bit more “normal.” That said, I learned a lot of lessons by not spending very much money back when I cared a lot more about having a high savings rate so I could build towards financial independence.

For you, I’d focus on housing and car expense. If you’re paying for daycare, you can’t do much about that. Perhaps you could move to where your support system is, but that’s not practical for most people.

If you’re really frugal with where you live and what you drive, you will be able to have a very high savings rate. If you get those two decisions right, you can splurge a bit on smaller items.

To organize your finances so you could hit a 50% savings rate or more, I’d suggest either

- Mint.com if you like the free option (they’ll hit you up with a ton of ads)

- Youneedabudget.com if you want to pay a small monthly fee for a better experience

- Our student loan consultant Rob has an underpriced service where he’ll help you figure out where all your money is going with his one hour, flat fee consult. This service is one of the best-kept secrets we’ve got

A couple examples of borrowers who could retire after getting huge loans forgiven

An OBGYN with $400,000 of student debt finishes her 4-year residency with $60,000 in her retirement account and $10,000 in her brokerage.

She moves to a middle of nowhere hospital in a state with no income tax and earns $400,000 per year.

She loses $100,000 to taxes, lives on $50,000, and invests the other $250,000 in a combination of retirement and taxable brokerage accounts. We’ll assume she earns an average of 7% a year while she’s growing her investments.

Year | Portfolio | Potential Income |

Year 4 | $70,000 | $1,600 |

Year 5 | $324,900 | $3,312 |

Year 6 | $597,643 | $5,144 |

Year 7 | $889,478 | $7,104 |

Year 8 | $1,201,741 | $9,201 |

Year 9 | $1,535,863 | $11,445 |

Year 10 | $1,893,374 | $13,846 |

When she receives loan forgiveness in year 10, she would have no more debt and would be able to live on about $75,000 per year based on the 4% rule.

How about a pharmacist who earns $100,000 per year, lives on about $30,000 and saves about $55,000 in investments annually?

Year | Portfolio | Potential Income |

Year 1 | $55,000 | $2,200 |

Year 2 | $113,850 | $4,554 |

Year 3 | $176,820 | $7,073 |

Year 4 | $244,197 | $9,768 |

Year 5 | $316,291 | $12,652 |

Year 6 | $393,431 | $15,737 |

Year 7 | $475,971 | $19,039 |

Year 8 | $564,289 | $22,572 |

Year 9 | $658,789 | $26,352 |

Year 10 | $759,905 | $30,396 |

Am I painting an unrealistic picture here? Perhaps, especially if kids are in the picture. However, if you have a partner or spouse who’s either providing childcare and cooking meals or working too, then you could save even more.

How can you reach financial independence and retire early without PSLF?

If you’re going to be paying for 20 or 25 years and owing a tax payment to the IRS, reaching FI is still possible.

You’ll need to project what you’ll owe to the IRS first using something like our calculator. Say it’s $300,000. You’d probably want to have $100,000 in an account today to have it grow into that amount over a couple decades.

Hence, whatever your “financial independence number” is, if you will have a tax bomb add about 10%. That’s going to cover your living expenses but also your tax bomb payment.

Want to be more conservative than that? Multiply the result of 25 times your expenses and add 20%.

Remember your payments are based on your income. Hence, if you retire early your payments might be as low as $0 a month.

What about health insurance?

Usually, people freak out when they don’t hear you talk about health care expenses in early retirement. Therefore, I must mention it.

If that family of 4 retired on $20,000 a year, they could artificially juice their income with Roth IRA conversions (and get access to retirement money early without penalty).

They would choose the right income to get maximum premium subsidies on a Silver Plan under the ACA. Their premiums could be as low as $0 a month, though they’d probably range between $50 and $100 per month.

Also, they would qualify for deductible assistance because of their income. This would limit their out of pocket maximum to no more than $5,200 a year even with that low premium.

Don’t like the ACA? You could always sign up for a Christian Healthcare Sharing Ministry like Liberty Healthshare or Samaritan Ministries.

I want you to think big even with student loans

When I make student loan plans for clients, it’s not my job to tell you what to do with your life.

I just want to make sure you know all your options.

Can you get student loan forgiveness after 10 years and retire early? A few people after seeing this math got motivated to save and invest more than they ever have before. They may or may not retire. That’s not the point. They’ll have the option to work how they want to.

When you owe more than $50,000 of student loan debt, having freedom is truly priceless.

What do you think of my math and discussion on how folks could retire early even with a huge amount of student debt? Comment below!

Can you please reword these to be sure I understand what you’re saying?

“Hence, whatever your “financial independence number” is, if you will have a tax bomb add about 10%. That’s going to cover your living expenses but also your tax bomb payment.

Want to be more conservative than that? Multiply the result of 25 times your expenses and add 20%.”

Thank you!