Disclaimer: This content is for informational purposes and isn’t meant to be investment advice. We recommend consulting with a financial advisor or other investment professional to ensure you understand how certain investments affect your unique situation.

Investment news usually stays under the radar.

But it seems like today, stories that are normally only covered on CNBC, Fox Business, Bloomberg TV, The Wall Street Journal, or the business section of your favorite news source, have made it into the regular news cycle.

GameStop, Tesla, Bitcoin, SPACs, Robin Hood. These are the top investing stories in 2021.

Heck, Travis, Molly and I even covered some of this on our Student Loan Planner® Podcast!

When stories like these become widely known to people who don’t normally follow investment news, and when people start jumping into the investment forum en masse, it can be a sign of a bubble.

But, are we in a stock market bubble? And if so, what’s causing it? Let’s dig in and see if we can get to the bottom of this.

What’s a bubble?

A bubble is when an asset price increases substantially without a justifiable increase in the underlying value.

In other words, the price is going up, but the investor isn’t getting that much in return for paying the higher price. It’s just becoming more expensive.

Investment bubble

As the investment sage Warren Buffett said, “Price is what you pay. Value is what you get.”

The goal of investing is to earn a return on your money for taking a certain amount of risk. Investors are willing to pay a certain price for an asset (stocks, bonds, ETFs, commodities, cryptocurrency, real estate, etc.) in return for what their investment could turn into over time.

Great investment returns generally come from paying a lower price than something is worth. This occurs when value is greater than price. Lower investment returns come when someone pays more than something is worth (i.e. price is greater than value).

What’s the value of an asset?

The best way to see how much something is worth (its value) is the expected future cash flow. This comes in the form of interest payments, dividends, and ultimately what you sell the asset for.

The more uncertain, risky, or costly the future cash flows are, the less an investor’s willing to pay for it. This is the basis of the discounted cash flow model to value an asset.

For example, let’s say you’re looking to buy a rental property, and you’re evaluating two properties at the same purchase price. In this scenario, you can charge the same amount of rent for each property.

However, one of them is in an up-and-coming neighborhood and you anticipate always having renters in there. The other property’s larger but it’s in an area where it could be a challenge to find consistent renters and collect rent.

Which one would you buy?

The answer is the one with more predictable rent. It has a greater value because of more certainty around collecting rent.

(One part I didn’t mention — to keep the example simple — is the expected price they could sell it at down the road. This also impacts the value of an asset.)

According to their value, these two properties shouldn’t be listed for the same price, but assets get mispriced compared to their value all the time. Sometimes they can be a great deal, other times they can be wildly overpriced.

That’s where spending time to do research comes in which goes out the window during bubbles.

Why do bubbles occur?

Investment bubbles have happened throughout history.

There’s a great book called Extraordinary Popular Delusions and The Madness of Crowds by Charles Mackay. This book was originally published in…1841 — that’s 180 years ago. It talks about bubbles and other mass hysterias in history.

One interesting chapter talks about The Dutch Tulip Bubble in the 1630s. At the peak, one tulip bulb was fetching 10x the annual salary of a skilled worker! Can you believe that it got that expensive?

Of course, the bubble burst and tulip bulbs dropped 99.9%+ in price within 2-3 years of the peak.

How on Earth could something get that expensive?

Mackay explains:

“We find that whole communities suddenly fix their minds upon one object, and go mad in its pursuit; that millions of people become simultaneously impressed with one delusion, and run after it, till their attention is caught by some new folly more captivating than the first.”

That’s a great way to think about bubbles.

2008 housing bubble example

The housing bubble that crashed in 2008 is a great example.

It started when Fannie Mae (Federal National Mortgage Association) had a noble goal to make housing more affordable and accessible. This loosened the requirements necessary to qualify for a mortgage.

With this increase in demand, prices started to rise.

Then interest rates went down leading to lower mortgage rates and monthly payments. This led to even more demand.

Homebuilders started building new real estate to meet demand. Banks got way too lax on their requirements of who could qualify for a mortgage. More and more people were buying houses, pushing prices up further and further.

Then came the flippers. Everyone and their uncle started buying, fixing, and flipping houses. It was “so easy” to make money. This was the last leg.

People started defaulting on their loans, banks who made risky loans ran out of money to lend, the faucet turned off and housing prices plummeted.

It’s hard to believe that was only 12 years ago. Remember, the real estate boom and bust also came right on the heels of the tech bubble burst in 2000 which again supports Mackay’s claim.

Why have asset prices gone up recently?

To me, the answer here is simple. Historically low interest rates that have lasted for a long time is why asset prices have gone up.

These low interest rates resulted in rising real estate prices, higher stock market valuations, and the search for other areas to find investment returns (cryptocurrency, NFTs, SPACs).

People with the cash and the means will look to invest in the best thing available. Keep in mind that there’s a lot more that goes into this, but I’m simplifying here.

How low interest rates make housing prices go up

When you’re looking to buy a house, do you look at the total cost or the monthly payment? If you’re like most, you just look at the monthly mortgage to see how it fits in your budget.

Let’s say you want to spend $2,500 for your mortgage (just the principal and interest, known as P&I).

How much house can you afford? It depends on the interest rate.

5% = $465,704 mortgage loan

3% = $592,973 mortgage loan

If mortgage rates went from 5% to 3% (which they actually did), the home buyer can “afford” a 27% more expensive mortgage for the same payment. Yes, the bank actually lends out $127,269 more money because it only looks at the payment, not the amount of debt.

That’s a clear example of how low interest rates make housing prices go up.

How low interest rates make the stock market go up

The stock market has historically done better than investing in bonds and holding cash over the long term. Part of the reason is the extra risk and price fluctuation associated with investing versus the cash stability in the bank.

Investors want a greater return to take the extra risk, so riskier assets should be priced to earn more than the stable assets.

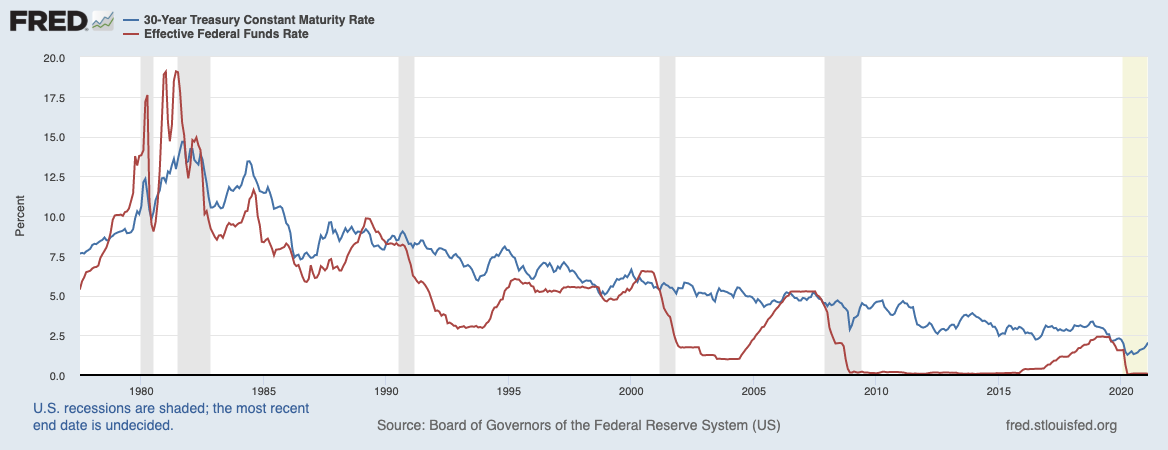

When I was growing up, I remember my savings account giving me 5% interest. The 30-Year Treasury Bond was paying 7% interest. The stock market average return at that point was 9% to 10%.

Today, we’re lucky to get 0.5% in a “high-yield” savings account and the 30-Year Treasury Bond is at 2%.

This begs the question, “Where can I go to earn more on my money?”

The answer: “Anywhere else!”

If you could earn 5% on your cash and 7% in bonds, you might be willing to take some risk in the stock market to earn 9%.

But when cash pays 0% and bonds are paying 2%, stocks might not need to earn 9%, maybe you think it would be enough if they could just return 5%.

If stocks were priced to return 9% while cash was 0%, everyone would be rushing to the equity markets which would push stock prices higher … and it has.

But what if your savings account started offering you 5% again and the market was priced to return 5%?

Wouldn’t you choose the safe cash rather than the volatile market for the same return? Why take the extra risk to get the same result? That’s another way low interest rates contribute to the stock market bubble.

Sidebar: Why’s the stock market going up when so many people are economically devastated?

There are a few reasons here.

First of all, the S&P 500 (the top 500 largest publicly traded companies by market capitalization) isn’t the economy. Approximately, 23% of the index is in only six of the 500 stocks: Apple, Microsoft, Amazon, Google, Facebook, and Tesla.

These companies are juggernauts. Their financial performance isn’t indicative of small businesses or gig economy, and have been performing well even during the financial crisis.

The second reason is that the government is pumping trillions of dollars into the economy. That flood of money is propping up the economy and asset prices.

The third reason is a global flight to quality. What if you live in a country with a dictator with rampant corruption or mass inflation or an unstable national currency? Bring your money to the U.S.! That global demand for quality drives more money into these investments which makes prices go up even more.

One other thing to note is that the stock market isn’t generally priced based upon what IS happening. It’s priced based on expectations of what MIGHT happen.

Case in point: the financial markets tumbled BEFORE the recession began in 2020 and rose as we were in the middle of the recession. There are plenty of other examples of this, too.

Related: How to Invest During a Recession

Why is everything else going up?

OK, so imagine cash is paying you nothing, bonds are low, the stock market seems high, and housing prices are going through the roof.

What do you do with your money now if you’re looking to make a decent return?

Find something else.

Enter SPACs, NFTs, cryptocurrency, the next investment du jour or asset class. Remember, banks, financial institutions, and companies might be sitting on cash and they’re looking to earn more money on their investments, too. Some of these products are creations that come from that.

Don’t get me wrong, just because there’s a bubble doesn’t mean that the underlying products have staying power.

The best example is the dot-com boom. There’s no question that it was indeed a technology revolution and the start of the internet era.

The market was right to get excited about the future of the internet, but prices just got crazy out of hand with astronomical expectations that they thought would continue for forever.

Are we in a stock market bubble?

If valuations are the #1 indication of a bubble, then yes. Right now people are paying huge prices and getting little value for what they’re paying. There are plenty of other signs, too.

The broad ranging media coverage, flocking to online trading, people thinking that investing is easy, and other asset classes skyrocketing.

Remember a bubble is when people are paying a high price compared to the value they’re getting in return. This has historically led to lower returns over time, and yes, I do think we can expect lower returns over time.

My guess is that when there’s a hint of interest rates going up or if the expectations of returning to “normal life” aren’t met, that could be the catalyst for asset prices declining.

Note that I didn’t say “when” it happens, I said when there’s a hint of it. Market prices are based on future expectations. Right now, those expectations are very rosy.

The thing about bubbles, though, is that they can go on longer than we think.

Yes, eventually a bubble will burst, but will it be a total collapse in a short amount of time or will it be a long drawn out period of low returns?

After the tech bubble burst in March 2000, it declined about 50% until bottoming out in 2003. Then, it went up 100% to match the March 2000 top in the fall of 2007 before tumbling again by 50% hitting bottom in 2009. The market finally made new highs in 2013.

That means that the U.S. Stock Market was essentially flat for 14 years (with a heck of lot of fluctuation in between). The same thing happened from 1968 to 1982 also, a flat market over that period.

There were individual pockets of the market that performed extraordinarily well during the 2000s but the overall market performance doesn’t show that. That’s what high valuations and a stock market bubble can look like.

It may take a while for the market to recover to the highs at the top.

What does investing for the long term look like if we’re in a bubble?

The key to wealth building has been consistently putting money to work over time. That starts by increasing your savings rate and investing at regular intervals.

This is also known as dollar-cost averaging. As prices decline, you can buy more for the same dollar amount.

Let’s say you put $1,000 per month away in a diversified mutual fund. When you start, you buy 100 shares at $10 one month. The next month, the price drops to $80, so you buy 125 shares with your $1,000. The following month, the fund recovers and you buy another 100 shares at $10.

The investment was right where it was when you originally bought it. But because you bought more at a lower price, your $3,000 investment is worth $3,250. That’s an 8.3% return in a flat market.

It’s like your retirement plan contribution. It happens regularly without thinking about it. 10 years later, you say, “Wow! How’d I do that?”

Look, no one can predict the market. Even the best of investors have made huge mistakes. Bubbles can last longer than we expect.

Related: How to Get Rich When You Can’t Predict 2021

If you’re new to the investment world, welcome! I love the democratization of investing. Pretty much anyone can start if they have a little bit of money, and I hope people continue to learn how to do it. That’s the way I started, too.

A word of warning though. My investing journey began during the 1998 to 1999 tech boom and I thought I was a genius until the bubble burst and I lost pretty much all of it in 2000 to 2001.

Just make sure that you’re funding your financial goals first before siphoning money off to invest on your own while you’re learning. Start small with an amount that you can “afford” to lose and won’t derail your financial aspirations.

Investing requires a ton of time which I didn’t realize while things were good and it seemed easy. But the upside is that it inspired me to learn more and pursue my CFA designation and a career as an investment analyst for the first 15 years of my professional life.

Whether we’re in a bubble or not, investing can work for those who systematically save and invest for the future. The market will rise and fall in giant waves. There will be humbling and frustrating times.

I believe (personal opinion), that investing is a great opportunity to build long term wealth, but you have to make the decision that’s right for you and your specific situation and risk tolerance.

By the way, Student Loan Planner® doesn’t manage, recommend or advise on investments and this isn’t meant to be any type of investment advice especially for your specific situation. This is just an opinion and perspective.

If you want to get a solid financial plan for your specific situation and develop an investment strategy that suits your unique needs outside of student loans, check out our financial planning resources.

Refinance student loans, get a bonus in 2024

| Lender Name | Lender | Offer | Learn more |

|---|---|---|---|

|

$500 Bonus

*Includes optional 0.25% Auto Pay discount. For 100k or more.

|

Fixed 5.24 - 9.99% APR*

Variable 6.24 - 9.99% APR*

|

|

|

$1,000 Bonus

For 100k or more. $300 for 50k to $99,999

|

Fixed 5.19 - 10.24% APPR

Variable 5.28 - 10.24% APR

|

|

|

$1,000 Bonus

For 100k or more. $200 for 50k to $99,999

|

Fixed 5.19 - 9.74% APR

Variable 5.99 - 9.74% APR

|

|

|

$1,050 Bonus

For 100k+, $300 for 50k to 99k.

|

Fixed 5.44 - 9.75% APR

Variable 5.49 - 9.95% APR

|

|

|

$1,275 Bonus

For 150k+, $300 to $575 for 50k to 149k.

|

Fixed 5.48 - 8.69% APR

Variable 5.28 - 8.99% APR

|

|

|

$1,250 Bonus

For 100k+, $350 for 50k to 100k. $100 for 5k to 50k

|

Fixed 5.48 - 10.98% APR

Variable 5.28 - 12.41% AR

|

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2024 on whether you should pursue PSLF, Biden’s New IDR plan, or refinancing (including the one lender we think could give you the best rate).