The answer can be fairly straightforward. It might make sense to refinance private student loans if you can:

- Get a lower interest rate.

- Lower your monthly payments (so you can focus on other debt).

- Take advantage of another lender’s favorable repayment terms.

It can be that simple, because unlike refinancing your mortgage where there are a ton of fees involved, there aren’t any closing costs to refinance your student loans. You might even qualify for a great cash-back refinancing bonus.

That makes it easier to decide whether to refinance private student loans because there’s no offsetting expense or “break even” point that has to be calculated. All savings flow right back into your pocket.

Even if you just refinanced six months ago, it might be a great idea to take a fresh look at refinancing, because student loan rates are near historic lows.

Benefits of refinancing private student loans

There are three main benefits of refinancing private student loans:

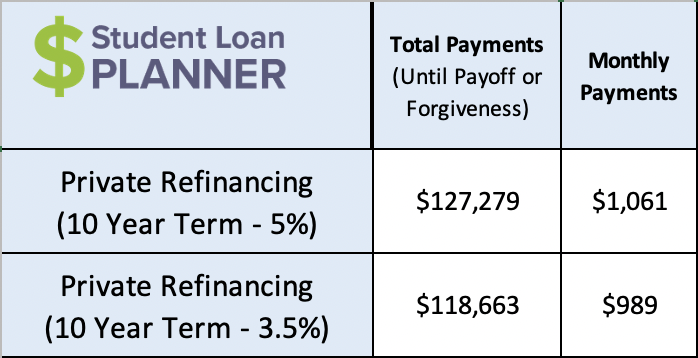

1. Save money on interest

Let’s say that someone has $100,000 in private student debt at 5% on a 10-year, fixed-interest rate. Today, they have the opportunity to refinance to 3.5%.

By refinancing, they’d save $8,616 in interest and are student-debt free in the same timeframe. Wouldn’t you rather have that extra money in your bank account? It’s a no-brainer.

2. Lower your loan payment

In the example above, refinancing private student loans lowers the payments on their student loan debt by $72 per month.

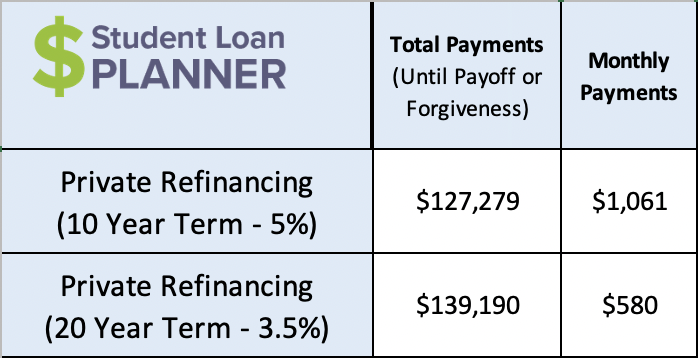

Now let’s say that you need to lower your loan payment because you had a drop in income, want to clean up credit card debt or build up an emergency fund in the meantime.

How would the payments change if this 10-year loan was refinanced to 20 years?

Going out to a longer term would lower payments by nearly $500 per month even with the original loan amount being the same.

Note: The goal is to pay off private student loans as quickly as possible, but if someone needs short-term relief, then a longer refinance term is a good option until they get back on their feet.

3. Change loan repayment terms and conditions

The primary reasons to refinance are interest rates and payment amounts, but other factors are also important.

For example, some lenders are offering a significant amount of forbearance — between 12 and 36 months. If your current private lender doesn’t have this option, then it might make sense to refinance to get those loan terms. This is assuming you’re not sacrificing the cost of student loan repayment.

Another reason is if you have a variable interest rate and it’s going to take you longer than three to five years to pay off your loan.

Fixed interest rates are better the longer the time frame you choose. So, if it’s going to take you more than five years to pay off the balance of your private student loans, swap the variable rate for a fixed rate.

For the reasons above and more, refinancing can be a great way to change your repayment options and get better loan terms.

How to refinance private student loans

Once you know that private loan refinancing is right for you, then it’s time to take a look at the different lenders out there.

They all might seem the same, but some offer better terms in certain situations.

Some lenders are better for healthcare workers while some offer unemployment protection. Some lenders find the best rates by going through community banks and credit unions, and some reward borrowers with a clean credit report.

Comparing your options across multiple lenders is worth the time. You never know if you can do better unless you check with a few lenders.

Here are the steps to refinance private student loans:

- Start by viewing today's top refinancing lenders that Student Loan Planner® partners with.

- Select three to five lenders to get preliminary rates. Click the links through our website and register with a new email address to potentially qualify for a cash-back bonus.

- Compare interest rates and terms across the lenders to see which offers you the lowest rates with flexible repayment terms.

- Choose a lender that gives you the best terms.

- Complete the student loan refinancing application online.

- Receive the final offer and accept it within 30 days, if the offer makes sense for your situation.

- The new lender you selected will pay off your old lender. You’ll then start making payments under your new loan terms with the new lender.

Quick note: Sometimes people get concerned that looking at more than one company will affect your credit score, but that’s not true. These preliminary rates are “soft” credit pulls which doesn’t materially affect your credit score no matter how many you do.

There’s also what’s called “rate shopping” when you explore many options over a 14 to 45 day period. During this window, multiple soft credit checks are counted as one on your credit report.

It’s worth it to check out as many as possible to make sure you secure the best interest rates and terms.

Should I refinance my private student loans?

You should explore refinancing your private student loans if you can get a better interest rate, need to adjust your required monthly payment, or recently had a nice jump in your credit score.

There’s no harm in checking even if you refinanced six months ago.

Remember, there are no closing costs so you don’t have to calculate a “break even” rate. If you can get even 0.25% lower, it’s worth it.

Just remember that if you have eight years to go and you refinance to a fresh 10-year term, you’re resetting the clock which could end up costing you more in interest. Even if the required payment is lower on the refinance, put as much money into it as you can (if possible) to get out of debt faster and pay less interest.

Remember step one: refinance your student loans through our site. Our partner lenders account for the vast majority of the student loan refinancing market. Plus, we take lower advertising fees from them to offer you some of the best cash-back bonuses out there.

We want you to save as much money as possible when you refinance your private student loans, so check out if you can get a better rate and qualify for a bonus.

Refinance student loans, get a bonus in 2024

| Lender Name | Lender | Offer | Learn more |

|---|---|---|---|

|

$500 Bonus

*Includes optional 0.25% Auto Pay discount. For 100k or more.

|

Fixed 5.24 - 9.99% APR*

Variable 6.24 - 9.99% APR*

|

|

|

$1,000 Bonus

For 100k or more. $300 for 50k to $99,999

|

Fixed 5.19 - 10.24% APPR

Variable 5.28 - 10.24% APR

|

|

|

$1,000 Bonus

For 100k or more. $200 for 50k to $99,999

|

Fixed 5.19 - 9.74% APR

Variable 5.99 - 9.74% APR

|

|

|

$1,050 Bonus

For 100k+, $300 for 50k to 99k.

|

Fixed 5.44 - 9.75% APR

Variable 5.49 - 9.95% APR

|

|

|

$1,275 Bonus

For 150k+, $300 to $575 for 50k to 149k.

|

Fixed 5.48 - 8.69% APR

Variable 5.28 - 8.99% APR

|

|

|

$1,250 Bonus

For 100k+, $350 for 50k to 100k. $100 for 5k to 50k

|

Fixed 5.48 - 10.98% APR

Variable 5.28 - 12.41% AR

|

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2024 on whether you should pursue PSLF, Biden’s New IDR plan, or refinancing (including the one lender we think could give you the best rate).