There are several programs available to federal student loan borrowers looking for help with repayment. It’s important to know how each option stacks up against the others.

Popular student loan income-driven repayment plans (IDR) with the U.S. Department of Education include Income-Based Repayment (IBR) and Pay As You Earn (PAYE). However, Income-Contingent Repayment (ICR) is also an option, and the new Repayment Assistance Plan (RAP) will be available in 2026.

What are the key differences between each program, and how do you determine which is right for you? Here’s what you need to know.

Income-driven repayment plan basics: Minimum required payments and years of repayment

Here's a quick comparison of each income-driven repayment plan's main benefits:

| Repayment plan | Payment (Based on discretionary income) | Timeline |

|---|---|---|

| Income-Based Repayment (IBR) | 10% to 15% | 20 or 25 years |

| Pay As You Earn (PAYE) | 10% | 20 years |

| Income-Contingent Repayment (ICR) | 20% | 25 years |

What happened to the SAVE plan?

Former President Biden established the Saving on a Valuable Education (SAVE) plan that allowed for more generous borrower benefits, including payments based on 5% to 10% of discretionary income, a larger poverty line deduction and an interest subsidy.

Unfortunately, the plan faced opposition from the beginning and is being phased out following a proposed settlement. Therefore, borrowers will be required to switch to another repayment plan.

PAYE vs. IBR: What's the difference?

With the PAYE plan, your monthly payment is based on 10% of your discretionary income. Your discretionary income is determined by taking your adjusted gross income (AGI) and subtracting 150% of the federal poverty line for your family size.

As for loan forgiveness, PAYE allows student loan forgiveness after 20 years of qualifying payments. However, to be eligible for PAYE, you must be a new borrower on or after October 1, 2007, and have received a Direct loan disbursement on or after October 1, 2011.

In comparison, under the IBR plan, your monthly student loan payments will be 10% to 15% of your discretionary income with 20- to 25-year loan forgiveness, depending on your loan disbursement date. Borrowers who took out their first loan on or after July 1, 2014, are eligible for New IBR, which offers more favorable terms than Old IBR.

It's also worth noting that the One Big Beautiful Bill Act removed the partial financial hardship requirement for IBR enrollment. Previously, borrowers whose Standard 10-Year payment was already affordable relative to their income could be denied IBR. That restriction no longer applies, making IBR accessible to a broader range of borrowers.

Note that there's an additional repayment plan: Income-Contingent Repayment (ICR). This plan's payments are based on the lesser of either 20% of your discretionary income or what you'd pay with fixed payments over 12 years. ICR forgiveness requires 25 years of payment. However, like PAYE, ICR is being eliminated and borrowers must transition off the plan by July 1, 2028.

For the purposes of this comparison, we'll focus on IBR and PAYE plans. However, it's worth noting that PAYE will not be available to borrowers who have any loans issued or consolidated on or after July 1, 2026, and will be eliminated for all borrowers by July 1, 2028.

Let's do some hypothetical loan simulator case studies for some of the occupations I see with large debt loads using our free student loan repayment calculator.

Our assumptions when comparing IDR plans

In the following hypothetical examples, I assume a 7% interest rate for the federal student debt and income increases of 3% for the folks we’re modeling.

For borrowers with loans originated before July 1, 2026, the aggregate borrowing cap is $138,500 for most graduate students (with higher limits for certain health profession programs).

However, under the One Big Beautiful Bill Act, new borrowers starting after July 1, 2026, face significantly lower caps: $100,000 for graduate programs and $200,000 for professional programs (such as medicine, law and dentistry), with Grad PLUS loans eliminated entirely for new borrowers.

I’m using the option of refinancing to a 10-year 5.5% interest rate as an alternative baseline to compare against.

Another big assumption is that schools would only charge the maximum borrowing limit for the cost of education. However, this could be wildly incorrect if they can convince the private sector lenders to start originating private student loans to cover the difference in revenues.

Finally, because I encourage all my clients to max out their retirement accounts, we’ll assume everyone is saving $24,500 a year in their 401(k) or 403(b) on a pre-tax basis. This strategy lowers student loan payments.

With each example, we pretend that our single borrower could choose between the PAYE and IBR plans.

We don't cover married borrowers in these examples. For borrowers who may need to consider a spouse's income or cases where you may be married filing separately, check out this post.

If you're a Parent PLUS loan borrower, head over to this post for help.

Want me to do a comparison for your specific situation? We offer one-on-one consultations.

Example 1: More debt than income

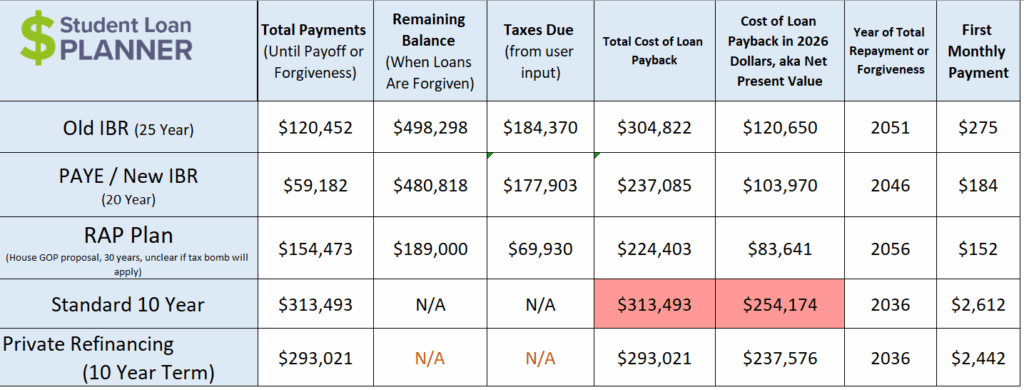

Let’s say Wendy is a veterinarian who graduated from the University of Pennsylvania and has way more debt than income. I currently see Penn alumni veterinarians come out with a loan balance of around $390,000 if their education was financed completely with student debt.

But let's assume Wendy has a federal student loan debt balance of $225,000 and works for Banfield Pet Hospital making $70,000 a year. Since she maxes out her pre-tax retirement contributions, her adjusted gross income is $45,500.

Let’s look at the cost of PAYE vs. IBR for Wendy's situation below.

Under PAYE or New IBR, Wendy's student loan payment amount would start out at $184 per month and adjust with her income and family size over time. She'd only pay back about $59,000 before having her remaining balance wiped away after 20 years of repayment.

However, if she isn't eligible for PAYE or New IBR due to when she took out her first loan, her payment under Old IBR would start at $275 per month. She'd also have to wait an additional five years to reach loan forgiveness, which would substantially increase her overall payback.

Either way, she'll likely have to pay a monster tax bomb on the forgiven amount. The tax-free treatment of IDR forgiveness under the American Rescue Plan Act expired at the end of 2025, so forgiven balances are now treated as taxable income. She'd need to start saving for that tax bill now.

Remember that your payments on an income-driven plan have little connection to your actual debt with the Federal Direct Loan program. Therefore, sticking with the Standard 10-Year plan or refinancing her student loans would be a suboptimal decision.

It’s difficult to look at the total cost column and make judgments without thinking about the cost of each path in today’s dollars. After all, these repayment periods are over different loan terms, and we need to adjust for alternatives where you could invest your money.

That’s why the relevant takeaway when looking at this chart is the cost in today’s dollars.

Example 2: Slim chance of repayment

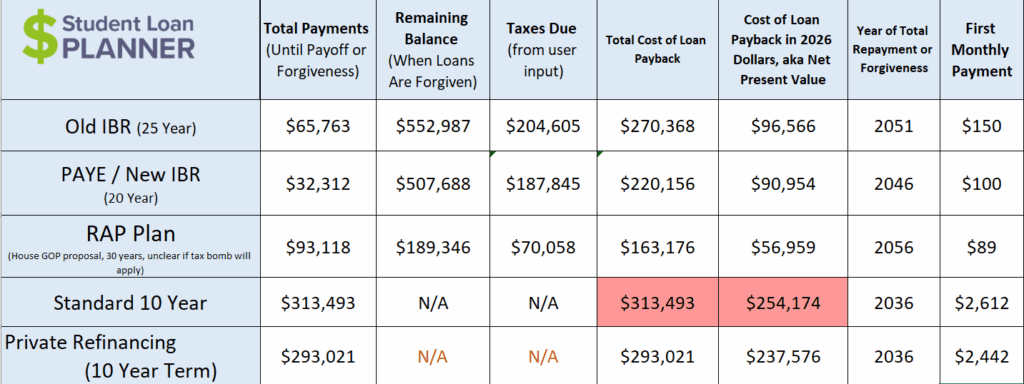

For this example, meet Jim, who is an associate chiropractor. Most chiropractors come out of school burdened by a ton of debt with incomes that are not all that different from what they could’ve made as non-specialized college graduates.

Perhaps this is due to the proliferation of chiropractors coming from private schools that charge a ridiculously high amount of tuition for the value of the degree.

Are there plenty of exceptions? Of course. I’m simply speaking in the aggregate.

Suppose Jim graduates from Palmer College of Chiropractic and becomes an associate for another doctor long-term. He brings in $60,000 a year and left school with about $275,000 of loans on the Direct Loan program.

This is what the cost looks like for each repayment option:

If Jim maxes out his retirement, his AGI would be $35,500. His federal student loan payments would start out at $100 under PAYE or New IBR versus $150 if he only qualifies for Old IBR. If his salary stays in line with a steady 3% increase every year and he continues to max out his retirement, he could benefit from significant loan forgiveness long-term.

Note that both plans will result in Jim owing taxes on the forgiven amount, since IDR forgiveness is now taxable income (the tax-free treatment expired at the end of 2025). He'll need to start setting aside money every month to prepare for that bill.

Example 3: Planning on Public Service Loan Forgiveness (PSLF)

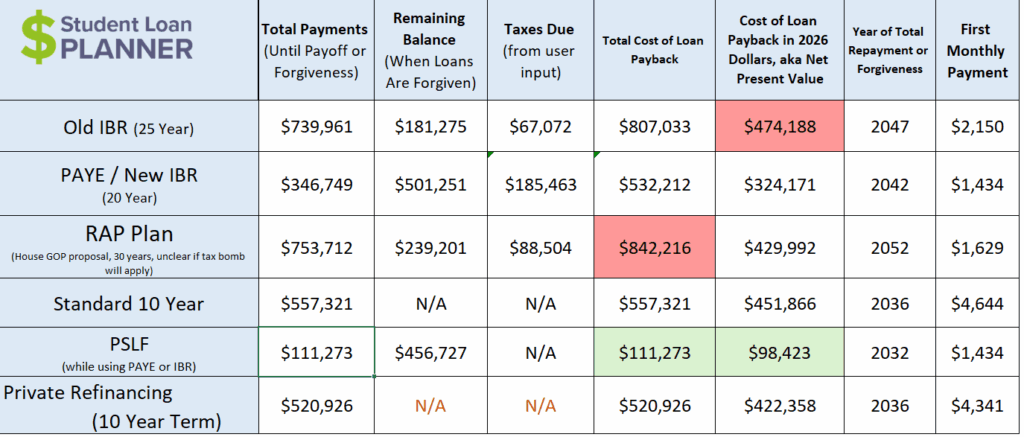

For this example, let’s use the fictional story of Christine, a doctor who plans to pursue Public Service Loan Forgiveness (PSLF). We’ll assume Christine is an OB/GYN resident who just graduated and will have an attending salary of $220,000. She works for a nonprofit hospital and qualifies for PSLF.

Let’s assume that under the Direct Loan program, she owes $400,000 from attending the University of New England College of Osteopathic Medicine.

We’ll also assume she has built up four years of credit toward forgiveness during residency.

After maxing out her retirement contributions, her AGI is $195,500. Her monthly payment amount would be $1,434 on PAYE/New IBR, and she'd qualify for forgiveness after 120 PSLF qualifying payments. That's right. All of her unpaid interest and principal will be wiped clean after ten years with no tax consequences.

Look at the massive difference between PSLF versus other IDR plans and private student loan refinancing. We're talking hundreds of thousands of dollars in savings by sticking with PSLF.

Example 4: High-income earners

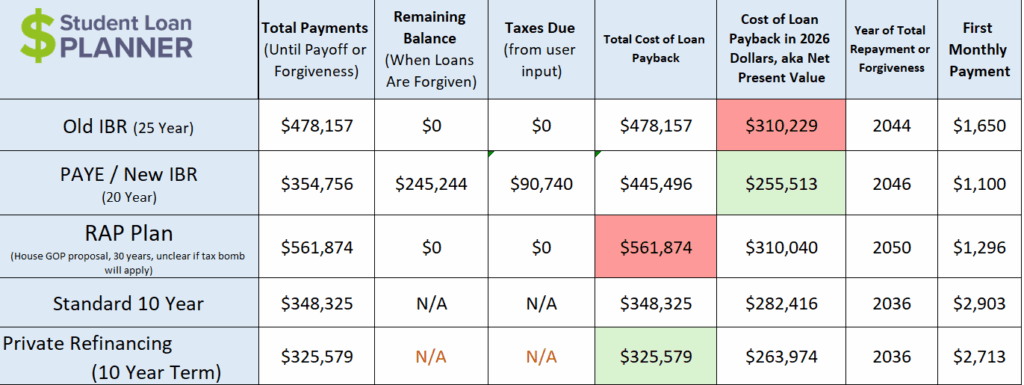

For our final example, let's assume Josh lives large in the big city. Although Big Law salaries increase at a rate much faster than 3%, let’s just assume for sake of simplicity that Josh, the Big Law attorney, went to the University of Virginia and has an annual income of $180,000 in New York City with inflation-level raises. He left school with about $250,000 of student debt under the Direct loan program.

By maxing out his retirement, he lowers his AGI to $155,500. Here are his repayment options for PAYE vs. IBR. We've also added refinancing for comparison.

Josh would have the lowest monthly payment under the PAYE/New IBR options. But he'd have to pay back loans over a long period and still have a tax bomb to deal with.

Choosing the best IDR or non-IDR repayment strategy

When it comes to student loans, there is no universal solution that works for everyone. Depending on individual circumstances, it may be best to pursue PSLF or long-term IDR forgiveness. In other cases, refinancing your student loans to obtain better repayment terms or lower interest rates may be the best course of action.

The best repayment strategy will depend on several factors, including your student debt and income. But it should also include your personal and professional goals.

If you currently have student debt from your undergraduate study or graduate school, we’re every bit as intense and analytical with each one of our client’s student debt consultations to make sure they have the best plan in place to minimize their costs. Set up a time to review your student debt situation with one of our experts.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.