Student loan interest can be a confusing topic. On the surface, student loans can look like any other installment loan, such as a mortgage or car loan.

For private student loans, that’s pretty much the case. But federal student loan interest can work differently than any other type of loan due to unique subsidies and repayment plans.

In this guide, we’ll take a deep dive into the mechanics of student loan interest for a variety of situations. Here’s how student loan interest actually works.

Understanding simple interest vs. compound interest

The nuances of student loan interest rely heavily on the differences between simple interest and compound interest. Interest rules depend on your loan type and your repayment plan. Let’s take a look at how the math works for both types of interest.

Note that for the examples below we'll assume that you have a fixed interest rate on your student loans. All federal loans come with fixed rates. However, your student loans could have variable rates if they were disbursed by a private lender.

How simple interest works

With simple interest, the interest rate is multiplied by the principal to find how much interest you’ll owe per year.

For example, with a $50,000 loan and a 5% simple interest rate, you’d owe $2,500 in interest per year ($50,000 x 0.05 = $2,500). And, over a 10-year period, your total interest accrual would equal $25,000.

Installment loans like mortgages, car loans, and personal loans typically use simple interest formulas. As long as you pay the loan as agreed, interest only accrues on the principal, not on accrued interest as well.

How to calculate compound interest

Compound interest works differently than simple interest. With compound interest, the interest you accrue is added to your balance each month, day or whatever frequency the lender sets. This is the formula for calculating compound interest:

Compound interest = P [(1 + i)n – 1]

Let’s define the various terms in the compound interest formula:

- P stands for principle

- i stands for interest rate

- n stands for the number of compounding periods

So let’s say you wanted to calculate how much compound interest you’d accrue on $50,000 in student loan principle with 5% interest compounded annually over 10 years. Here’s how you’d use the above formula to find that number.

Compound interest = P [(1 + i)n – 1]

$50,000 [(1 + 0.05)10 – 1]

$50,000 [0.6289]

Compound interest = $31,445

So we see that using a compound interest formula resulted in an extra $6,000 of total interest when compared to the simple interest calculation.

And, remember, in our example we assumed that interest would compound annually. With more frequent compounding schedules, the differences would be even more pronounced.

How student loan interest actually works

Student loan interest generally compounds on a daily basis. But, before you panic, that doesn’t mean your balance will be growing each month (as can happen with credit cards).

If you pay your federal loans according to the 10-Year Standard Repayment Loan or your private loans according to your loan terms, your loan balance will only go down over time and you won’t accrue unpaid interest.

But what about times that you’re not paying toward your student loans, like during school, during a grace period, or during a period of forbearance? In many cases, interest will continue to accrue during these periods.

When you begin repayment, that accrued interest may capitalize, which means it would get added to your principal balance. So, from that point forward, you will be paying interest on your interest.

How student loan interest works on income-driven repayment plans

Federal student loan income-driven repayment (IDR) plans offer a unique benefit that isn’t available with private loans.

On an IDR plan, unpaid interest does not capitalize as long as you’re on the plan. Instead, simple interest is charged on your outstanding principal at all times.

This detail is a big deal. Many borrowers on IDR plans may not even be paying enough each year to cover their interest charges. With a typical repayment plan, this unpaid interest would capitalize and get added to your principal. But with IDR plans, your annual interest accrual does not increase over time.

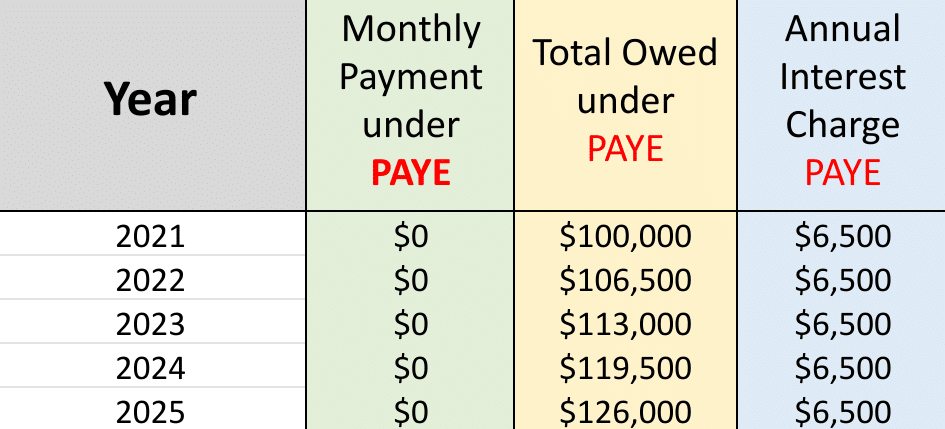

Your effective interest rate can decrease over time

For example, imagine that you have $100,000 in student loans at a 6.5% interest rate. You’re on the PAYE plan, and your monthly payment amount is $0. In the first year, you’d accumulate $6,500 in interest. And that’s exactly the same amount of interest you’d accumulate in year-five.

So, even though your balance would be growing, your annual interest charges would remain the same.

This means that your effective interest rate actually goes down as your student loan balance goes up on an IDR plan.

How student loan interest works if you qualify for a subsidy

In certain situations, students may qualify for subsidies that can reduce their student loan interest accrual. Here are the two most common types of student loan interest subsidies:

1. Subsidies for specific student loans

Some student loans do not accumulate interest while the student is in school. For example, with Direct Subsidized Loans, the Department of Education pays your student loan interest for you while you’re in school and during your six-month grace period.

Note that only undergraduate students are eligible for subsidized loans. And even undergrads will need to demonstrate financial need on their Free Application for Federal Student Aid (FAFSA) to qualify. Subsidized student loans also have lower borrowing limits than other federal student loan options.

Some loans that are specifically designed for certain professional students may also offer this benefit. The Health Professions Student Loan Program is a prominent example. These loans do not begin to accrue interest until after the student has graduated and a one-year grace period has elapsed.

Student loan interest on other federal student loans

You won't receive the benefit described above on a Direct Unsubsidized Loan, PLUS Loan, or Direct Consolidation Loan. With these student loans, interest will begin accruing immediately, even if you aren’t required to make payments until after you graduate.

That accrued interest will be added to your balance once repayment begins. You can avoid this potential financial impact by making interest-only payments while you’re in school.

2. Subsidies for specific repayment plans

Some IDR plans offer student loan interest subsidies as well. With the PAYE and IBR, the government will pay all of the unpaid interest on your subsidized student loans for the first three years of your repayment.

But the new SAVE plan (formerly REPAYE) has more generous benefits than any other IDR plan, including interest benefits that stop your subsidized and unsubsidized loan balances from growing.

Interest subsidies on the SAVE plan

The SAVE plan is the real star of the student loan interest subsidy show. For borrowers on the SAVE plan, the government will cover 100% of any remaining monthly interest for both subsidized and unsubsidized loans if you make the full monthly required payment.

Pretend your loans accumulate $100 in interest each month and you have a required $50 monthly payment. The remaining $50 would be eliminated once you make your scheduled monthly payment on time.

This special benefit makes SAVE a great option for borrowers who are looking to maximize IDR student loan forgiveness.

Student loan interest FAQs

How often is interest added to student loan balances?

Students loans generally accrue interest on a daily basis.

When you’re paying down your loans, the amount of interest you pay each month will go down. But during periods of non-payment, your student loan interest can compound each day.

How much of my loan payment is interest?

The amount of your payment that goes toward interest is highest at the beginning of your amortization schedule. But it goes down over time.

Borrowers can accrue unpaid interest during forbearance or deferment periods. If you’ve accrued unpaid interest, your payment will be applied toward that outstanding principal balance. For this reason, 100% of your student loan payment could go toward interest in some cases.

How can I avoid paying interest on student loans?

When a student loan is in normal repayment, it’s impossible to avoid interest charges completely. But borrowers can reduce the interest they pay over the life of the loan by refinancing to a lower interest rate.

Students can also make interest-only payments during periods of non-payment, like during academic deferment and grace periods. This can minimize interest capitalization later after the student graduates and begins normal repayment.

How do I calculate my student loan interest?

To calculate your student loan interest, follow these steps:

- Divide your annual interest rate by 365 to find your daily interest rate.

- Next, multiply your daily interest rate by your principal to find your daily interest charge.

- Next, multiply that amount by your billing cycle (typically 30 days).

- Finally, multiply that number by 12 to get your annual interest cost.

How do student loan interest subsidies work?

Student loan subsidies allow borrowers to avoid unpaid interest being added to their principal.

With Direct Subsidized Loans, the Department of Education pays unpaid interest on the student’s behalf. Borrowers may qualify for student loan interest subsidies by getting on an IDR plan. For example, borrowers enrolled in the SAVE plan receive an interest subsidy that covers any remaining monthly interest that isn't covered by your monthly payment.

Get answers to more questions about your student loans

Student loan interest works like a normal loan if you’re making payments (either to the government or a private lender) according to the normal schedule. However, there are important differences that don’t exist with other kinds of debt.

You could be dealing with simple interest, compound interest, or subsidized interest depending on what kind of repayment plan you're using and what your income is.

If you look at traditional debt repayment advice, you need to understand the unique student loan rules or you could make a mistake.

We're the student loan experts. Talk to our professionals for advice on how to minimize your interest cost. Book a consultation today.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.