According to the American Dental Association (ADA), the average first-year cost of dental school is $46,865 for residents, $76,060 for non-residents and $87,078 for private school. And those averages don't include living expenses. The American Dental Education Association estimates the average indebted dental student in 2025 graduated with $297,800 in dental student loans.

Perhaps even scarier, four in five dental students graduate with debt. Sadly, those massive debt profiles do not even tell the full story.

Many dentists have to borrow even more after obtaining their DDS or DMD for tuition and fees during residency or other postgraduate specialty training.

To top it off, compound interest growth from forbearance and deferment during this training can easily result in a $400,000 to $600,000 student loan balance before newly minted dentists even earn their first “real” paycheck.

Pardon the pun, but dental student loans are drilling the future of the profession. In this article, we'll explore why and discuss the best loan repayment options for dentists.

How dental student loans can grow to massive sums

The best way to visualize the educational debt problem facing dental students is with an example. Assume Tim graduates from a private out-of-state dental school without any grants or scholarships. After tuition, fees, and living expenses, he needs to borrow $75,000 each year over the four-year program.

Most of his loans will be unsubsidized meaning that the interest accrues every year he's in dental school at an average interest rate of 7% interest (the interest rates on federal student loans vary each year). I estimate his balance will be approximately $330,000 at graduation, of which $30,000 is accrued interest.

Now, Tim decides to complete a post-graduate program in pediatric dentistry with a two-year cost of $20,276. Because Tim earns a low stipend, he decides to use forbearance for his student loan balance. His dental student loans now grow at a compound interest rate of 7%, and he adds further loans to the total balance.

Here's a look at what his first year of postgrad training would look like:

| Year 1 loan balance at beginning of postgrad training Year 1 tuition and fees Year 1 interest growth | $331,500.00 +$20,276.00 +$24,624.32 |

| Year 2 loan balance at beginning of postgrad training | $376,400.32 |

As Tim enters his second year of postgrad training, his loan balance grows even more:

| Year 2 loan balance at beginning of postgrad training Year 2 tuition and fees Year 2 interest growth | $376,400.32 +$20,276.00 +$24,624.32 |

| Loan balance upon completion of training | $424,443.66 |

Now Tim's loan balance stands at $424,443.66. Keep in mind, this massive sum assumes he has no undergrad debt. If Tim went to a moderately priced four-year college and came out with $50,000 of student loan debt from that degree program, the debt would be over $500,000 in total.

Confusion leads to many dental loan repayment mistakes

In my student loan consulting business, I've heard high income dentists say that they decided to join an Income-Driven Repayment (IDR) plan, simply because they hoped they would receive some form of student loan forgiveness. Unfortunately, most dentists do not understand the consequences of that forgiveness.

Dental incomes are low enough after taxes that it's very difficult to pay down a huge balance rapidly. However, they are also high enough that monthly income-based payments are large. Therefore, most balances will eventually be repaid over 15 to 20 years before they're eligible for forgiveness programs.

If, by some chance, there's a balance remaining to be forgiven, it could be treated as taxable income. Due to COVID-19, there was a temporary suspension on taxes for loan forgiveness. But that suspension expired on December 31, 2025. That means if you receive forgiveness in 2026 or beyond, the IRS could expect a balloon tax payment on what could be hundreds of thousands of dollars.

Additionally, the pain of deferred gratification means many dental school graduates make a few large purchases a few months into receiving their first large paycheck. These income and spending realities further reduce the ability of dentists to pay large sums towards their debt.

IDR plans are not all created equal

Most dental school grads will use the IDR program recommended by their financial aid office or loan servicer. And that recommendation usually sounds something like: “This is what most people do.” But IDR plans vary based on eligibility rules, income calculations and forgiveness timelines — and picking the wrong one can cost you hundreds of thousands of dollars.

Let's go back to Tim from our earlier example.

During his pediatric dentistry program, Tim got a quick explanation of his repayment options and moved forward with the plan that seemed simplest. Like many borrowers, he didn’t compare how each option would play out over 20 or 25 years. We will also assume that he got married during his pediatric dentistry program and started a family. He and his wife have 2 children together and are not planning to have any more. To simplify the modeling, we'll say his wife stays home with the kids and does not earn an income or have student debt herself.

We also assume that he starts out at $196,000 in total compensation. To account for increasing earnings over time, let's say Tim's pay grows at a rate of 3% per year.

This is where the gap between “standard advice” and actual strategy becomes expensive.

Financial aid offices and loan servicers are helpful for getting loans set up, but they’re not typically modeling long-term repayment outcomes.

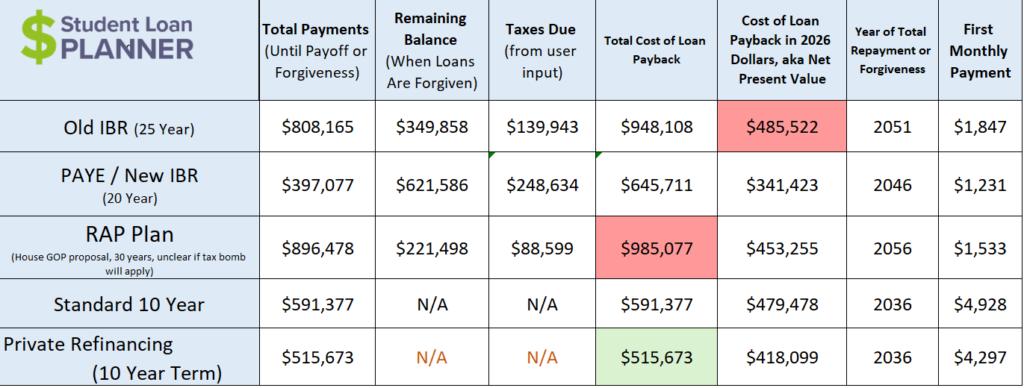

Based on existing IDR plans, Tim's realistic options include PAYE/New IBR, Standard 10-Year Repayment and private refinancing.

Note the new Repayment Assistance Plan (RAP) is included for reference, but it isn't expected to go live until July 2026. Because key details are still evolving, these results should be viewed as projections based on what we know today.

We'll assume that Tim would owe a combined federal and state marginal income tax rate of 40% on forgiveness. Here are the total costs below.

Notice that the total cost of repayment for Tim’s dental student loans is over $645,000 under PAYE/New IBR, which makes them the least expensive federal repayment options available to him while still keeping his monthly payments low early in his career.

Note that PAYE is scheduled to be phased out by June 30, 2028. As long as Tim qualifies for New IBR, that would likely be his best long-term federal option. If he borrowed before July 1, 2014, he could be choosing between PAYE and Old IBR. In that case, PAYE would offer lower monthly payments since it’s based on 10% of discretionary income versus 15% under Old IBR. However, he would need to plan to switch to IBR before PAYE sunsets, which introduces some risk if he’s not closely tracking student loan changes.

Best loan repayment options for dentists

Ok, so I think I've done a thorough enough job of highlighting the debt problems that many dentists face. But now let's move on to the solutions. Here are some the best loan repayment options for dentists.

Income-Driven Repayment: Best while you're in residency or postgraduate training

For most dentists, using an IDR plan during residency or postgraduate training is the best move. These plans are available for borrowers with federal Direct Loans and are designed to keep payments low while income is limited.

Today, that typically means using New IBR or PAYE (while it’s still available), depending on eligibility.

If a dental resident can qualify as a full-time employee, their monthly payment could be as low as $0 a month depending on the size of their family and the size of their stipend.

So with Tim's wife staying at home, their payment would be very low. Most dentists make major mistakes by using forbearance or deferment during postgraduate dental programs. That approach allows interest to grow unchecked and can significantly increase the total cost of repayment over time.

The choice of repayment plan should be made on a case-by-case basis. However, starting payments as soon as possible is a good rule for everyone to use. Even a couple hundred dollars per month would slow the growth of interest.

Student loan refinancing: Best once you're earning a “real” paycheck

As you can see from the analysis above, private refinancing results in the lowest total cost in this scenario. Tim will save thousands of dollars using this strategy. He will also save that money on an after-tax basis.

Unlike mortgage interest, student loan interest is not tax deductible for all intensive purposes. To come up with $100,000 to pay student loan interest, dentists have to earn about $180,000 to $200,000 in pretax income. That $645,711 of PAYE/New IBR repayment plan cost translates to roughly $1.2 million in pretax income.

The extremely high cost of student loan interest for dentists means that many should consider refinancing their student debt. I will include links at the end of the article if you want to check your rates. It takes about five minutes to get an immediate offer online, and it doesn't affect your credit.

Most dentists have high incomes and therefore strong cash flow above basic living expenses. Because of this, many would qualify for fixed and variable rates much lower than what most dentists have on their Direct Grad Plus and Direct Unsubsidized student loans.

Do refinanced loans still qualify for loan repayment assistance programs?

Yes! For dentists that happen to work for a qualifying employer or in an eligible community, there are several loan repayment programs they can qualify for regardless of loan type. Here are few popular examples:

- National Health Service Corps (NHSC) Loan Repayment Program: This program offers up to $50,000 of loan repayment for dentists and other medical professionals who commit to working in a Health Professional Shortage Area (HPSA) for a service obligation of at least two years. The maximum award is $25,000 for half-time workers.

- National Institutes of Health Loan Repayment Programs: Eligible candidates (includes dentists, primary care physicians, and clinical pharmacists) can have up to $50,000 of their loans repaid per year in exchange conducting mission-relevant research.

- VA Education Debt Reduction Program (EDRP): With this program, you can receive up to $40,000 per year of educational loan repayments for up to a five-year award amount of $200,000. Dentists and other healthcare professionals are eligible provided that they agree to work for the VA in a difficult-to-recruit, direct patient care position.

- Indian Health Service Loan Repayment Program: The IHS Loan Repayment Program will pay up to $50,000 towards the student loans of eligible dentists (and other health professionals) who serve American Indian or Alaska Native communities.

None of these programs require borrowers to have federal loans to qualify. You will lose eligibility for the Public Service Loan Forgiveness program (PSLF) by refinancing. But, as we'll see below, there's a strong chance that you won't qualify for PSLF anyway.

What about Public Service Loan Forgiveness (PSLF)?

Dentists get the short end of the stick under current student loan programs. To see why, in detail, consider an example I used in an article showing the incredible student loan options available for doctors.

But the short explanation for why dentists are given such a raw deal is that the Public Service Loan Forgiveness program categorizes not-for-profit hospitals as “qualifying employers.”

Many physician residencies and fellowships meet the “qualifying employer” criteria. Doctors have lower incomes during postgraduate training, which results in low monthly payments. These payments all count towards the 120 monthly payments required to have an entire student debt balance forgiven tax-free under the PSLF program.

In contrast, dentists do not have access to widespread government or not-for-profit jobs. The vast majority of dentists work for private employers. The reason is because of the structure of the Medicaid and Medicare program. The federal government just does not provide massive funding for dental care.

That means doctors have access to an incredibly valuable student loan loophole. A huge percentage of them will pay five figures to wipe out six figures of student debt.

Dentists have more options than other professions

Repaying dental student loans is an arduous task. However, my consulting experience has shown me that dentists should be hopeful. Looking at the issue from the “glass half full” perspective, the loan repayment options for dentists are much better than for other professions.

Contrast dentists with veterinarians, many of whom graduate with debt-to-income ratios above three to one. At that debt-to-income ratio, many people give up hope and just let the debt spiral out of control. With veterinarians, I have to come up with ways to optimize the government loan repayment programs. I also have to prepare them for a massive six-figure tax bill in 20 to 25 years. That is the only option available in many cases.

In contrast, most dentists qualify for a private refinancing option because of higher incomes. Even borrowers with DTI ratios of almost two to one sometimes get rates as low as 4.5% to 5.5% (depending on interest rate environment). If your debt-to-income ratio is below 1.25, you could qualify for an even lower interest rate.

The average dentist could save tens of thousands on student loan payments

Are dentists unfairly treated under student loan policy? Absolutely. However, you have options. Often, using private refinancing can save you thousands of dollars in interest. I have negotiated referral agreements with the top lenders in the marketplace that could help. These companies pay a refinancing bonus that is not available if you just visited their site directly.

Private companies do not offer PSLF or income-based repayment, but they often result in much lower interest charges. If you're a private practice dentist, refinancing could be your best options once you start practicing. Feel free to check your rates with the links below.

I hope I've given you a decent education about the best loan repayment options for dentists. If you would like me to analyze the different offers and make sure private refinancing is the best option compared to optimizing an IDR you can hire one of our student loan advisors. Book your student loan plan here.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.