Recertifying your income-driven repayment (IDR) plan for Pay As You Earn (PAYE), Income-Based Repayment (IBR), or Income-Contingent Repayment (ICR) can open up opportunities to pay less if you're pursuing PSLF or IDR student loan forgiveness.

Since federal student loan payments resumed in October 2023, borrowers have encountered a wide range of confusing and inconsistent guidance about recertification dates due to administrative delays and program changes. The most recent extension moved recertification deadlines to at least February 2026. That said, timelines aren't uniform. We've seen some borrowers with recertification dates as far out as 2027, while others received bills demanding prompt payment.

The key thing to know is when to turn in your income recertification. If you turn in a higher income too early, you could unnecessarily pay thousands in extra payments. If you fail to inform your servicer about a drop in income, you could also cost yourself thousands.

We'll share some great tips on paying less on your IDR payments by making this income-driven recertification decision correctly.

When is IDR recertification due?

Your annual recertification is typically within a year of choosing an IDR plan as one of your repayment options. The payment pause during the pandemic put this on hold, followed by various recertification date extensions under both the Biden and Trump administrations. These extensions and processing mishaps have caused confusion but have also resulted in many borrowers not having to recertify until sometime in 2026 or later.

Having extra time is huge news and means you might be waiting a while before your servicer asks you for your income information and family size.

You can find your recertification due date on your StudentAid.gov dashboard or by downloading your NSLDS data file from the Student Aid website.

How to know if you should recalculate your IDR payment

In most cases, borrowers are better off waiting to recertify until their servicer requires it. However, you'll want to recertify early in general if your income has fallen compared to the last time you provided your tax return. This might be the case if you've reduced your hours or experienced job loss.

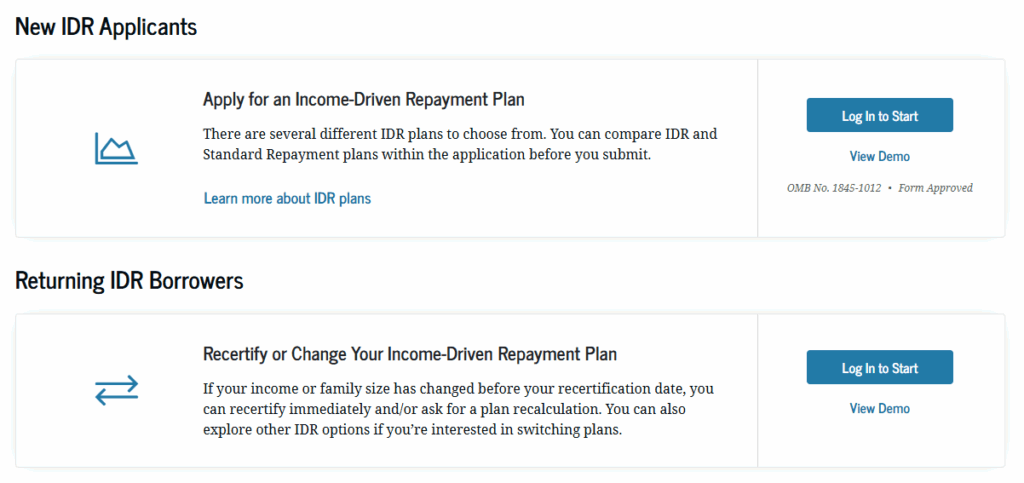

To apply for early IDR recertification, simply visit the StudentAid site and click on the appropriate button for “Recertify or Change Your Income-Driven Repayment”.

For many borrowers reading this, that tip will be the single most important piece of student loan advice you read anywhere for the next year.

If your current income is lower than before or your family size has increased, you can expect a lower IDR payment.

Remember that you are not required to let the Department of Education know if your income has risen. That's all handled by submitting your tax return each year. Recertifying early with a higher income can unnecessarily increase your payments and overall costs, particularly if you're pursuing PSLF or long-term IDR forgiveness.

How IDR recertification can save you money

First, figure out your next IDR recertification date for your federal loans. You can do this by contacting your federal student loan servicer and asking, downloading your NSLDS file and looking at it, or by hiring Student Loan Planner® to make a plan for your student loans.

If you haven't recertified your income recently, your current IDR payment will be based on the last income information your servicer has on file. And that payment will last until your next scheduled IDR recertification date.

If you could get a lower payment by recertifying early, then you should do so. You might be able to figure this out through our online calculators.

How to get lower IDR payments if you have increasing income

If your income has increased recently, the main thing to focus on right now is timing.

If your IDR recertification date falls before your current-year tax return is due, you may be able to use the prior year's lower income instead. That way you can keep your payment lower for another year.

One way to preserve that flexibility is by filing a tax extension. An extension delays the filing of your new return, allowing your loan servicer to use your previously filed return when calculating your payment.

For example, if your recertification date is coming up in 2026 and your 2025 income is higher than the previous year, filing a 2025 tax extension could allow you to use your 2024 tax return for income documentation.

This strategy is also important for borrowers transitioning out of SAVE forbearance or switching to another IDR plan right now, since you'll be required to provide updated income information regardless of your official recertification date. For borrowers who haven't recertified in recent years and are earning more money than before, that could result in a significant payment increase.

Timing matters. Depending on your situation, strategies like filing an extension or filing taxes separately to exclude spousal income may help reduce your required IDR payment.

How to get lower IDR payments if you have decreasing income

If your income dropped, you simply need to visit the Student Aid site I linked to above and click “Recertify or Change Your Income-Driven Repayment” to recalculate your monthly payment based on current income. Just be prepared to provide alternative income documentation, such as pay stubs, an employer letter or a signed statement explaining your income situation.

Many borrowers will fail to do this, and it will collectively cost them millions of dollars.

If in doubt about IDR recertification, wait until asked

If you’re unsure when to recertify your IDR, just wait until you’re asked to do so.

For many borrowers, recertifying early can increase monthly payments, especially if income has risen since the last time income documentation was submitted (which in some cases may have been years ago).

However, early recertification may make sense if your income has declined since your most recent certification, or if you could benefit from filing taxes separately.

But if your income has increased, look at your recertification timeline before filing your next tax return. In some situations, filing a tax extension can help preserve lower payments by allowing you to use a lower-income return for another year.

Be ready and have a strategy so you can either refinance to lower rates or pay as little as possible with the help of a team like ours.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.