Refinancing can be a great way to reduce your interest rate and the cost of your student loan pay-back. It’s a process where you take your federal student loans or your existing private student loans and replace them with a new private loan to lower your interest rate and/or change your loan terms.

But what if, due to your credit score, you don’t get approved for an interest rate lower than some of your existing interest rates?

“Does it make sense to refinance part of my student loans?” I get this question all. the. time. The short answer is yes. But should you? Let’s dissect it.

NOTE: Refinancing is different from consolidation. A Direct Consolidation Loan combines multiple federal education loans into one federal loan, keeping them within the federal system. Consolidation doesn’t improve your interest rate, but it doesn't really make the interest rate worse either. Consolidation takes the weighted average of your existing loans and rounds up to the nearest 1/8th of a percent.

When folks graduate, they usually have a laundry list of loans since financial aid is issued each semester. For federal loans, you can also have two different types of loans issued each semester as seen on the loan file below.

When you borrow federal loans, you lock in a fixed interest rate which won’t change over the life of the loan (unless you refinance or consolidate in the future), but each following year the interest rate can change as you continue to borrow. Interest rates on federal student loans aren’t set by the U.S. Department of Education — they’re set by federal law, annually.

In the loan file above, interest rates range from as low as 3.4% all the way to 7.21%. If this person consolidated, their weighted average interest rate would be 6.14% which is rounded up to the nearest 1/8th of a percent. Their final interest rate would be 6.25%.

One might say, “Wow that’s a high interest rate… you should refinance!” But not so fast — student loan repayment planning isn’t just about the interest rate.

This person has $152,000 of federal student loan debt and has been on PAYE since 2016. They make $62,000 per year and are married, but filing taxes separately, to keep the payment off of their own income:

Continuing the taxable forgiveness route on PAYE is optimal. If this person refinanced and lowered their interest rate down to 4%, their monthly payment would more than triple and they’d pay a total cost of $49,669 MORE than if they’d stay on PAYE and save for the tax bomb.

I’ll say it again: it’s not just about the interest rate.

But does it make sense to refinance high-interest student loans only? Let’s tease this thought out. Let’s say we refinanced all of the loans over 6.5%, and kept the rest federal.

The loans over 6.5% totaled to $59,091, leaving $93,037 left. If we stayed on PAYE with those, the following would play out:

PAYE is still the optimal path for the remaining federal loans but you’ll notice that the “Total Payments” column (the total monthly payments made between now and forgiveness) is the exact same total as our original path keping all the loans federal. The tax bomb changes, but not how much they pay into the federal system.

How can that be? This person would still be on pace for the taxable loan forgiveness and PAYE keeps their payment based off of their income, not the balance or interest rate at all. So not only does refinancing not reduce the amount they’re paying to the federal system, it also adds another bill into the equation:

If they got that interest rate down to 4% and stuck to the same timeline to pay off the loans as PAYE would reach forgiveness, this person would pay:

- $78,676 for their private loan pay off

- $59,974 into the federal system for their monthly PAYE payments

- $47,502 tax bill for the forgiven balance on the federal loans in 2036

= $186,152 total cost

Compared to a total cost of $152,880 on the first example, staying the course on PAYE for all the loans.

This example boils it down to one truth: if you have federal loans and you’re a clear case for IDR or PSLF forgiveness, refinancing some of your federal loans doesn’t benefit you.

Let’s look at another example where someone is NOT a forgiveness case.

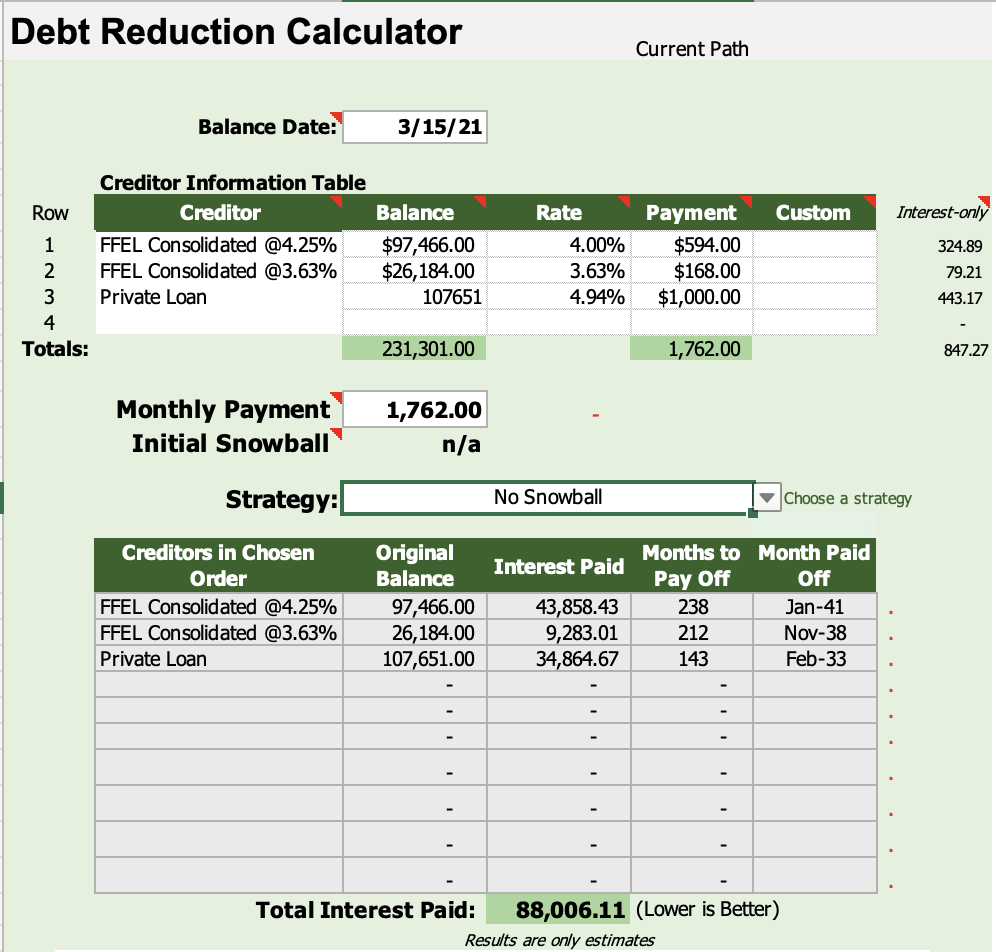

This next person has both federal loans (listed below) and private loans at a total of $107,651 at an interest rate of 4.94%.

This person wasn’t a good candidate for longer term forgiveness based on their income so paying these off sooner rather than later is more optimal. Their federal interest rates are pretty darn good already though! What’s the plan of attack?

The easy answer is refinance and hope you get an interest rate lower than all of your existing interest rates — in this case, 3.63%. But what if this person got approved for only 4%?

You could cherry pick and keep the 3.63% loans out of the refinance to preserve their lower rate but that would mean two different payments and two different pay-off timelines, possibly. And is it mathematically worth it to keep them out?

Let’s first establish what their current path looks like. If they kept the course with no snowball (kept paying only the monthly payment due on each loan until it was paid off):

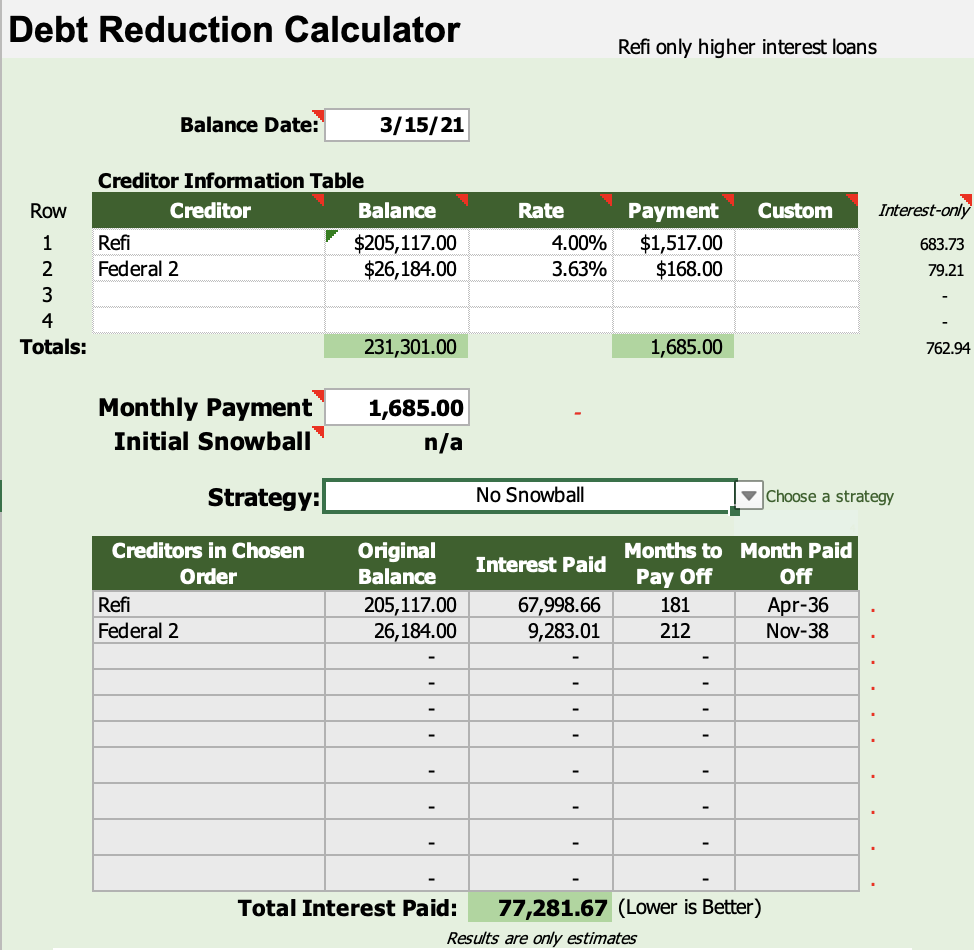

Let’s compare to if they refinanced just the loans that were over 4% on a 15-year term (keeping the payment somewhat comparable to their current payments) with no snowball:

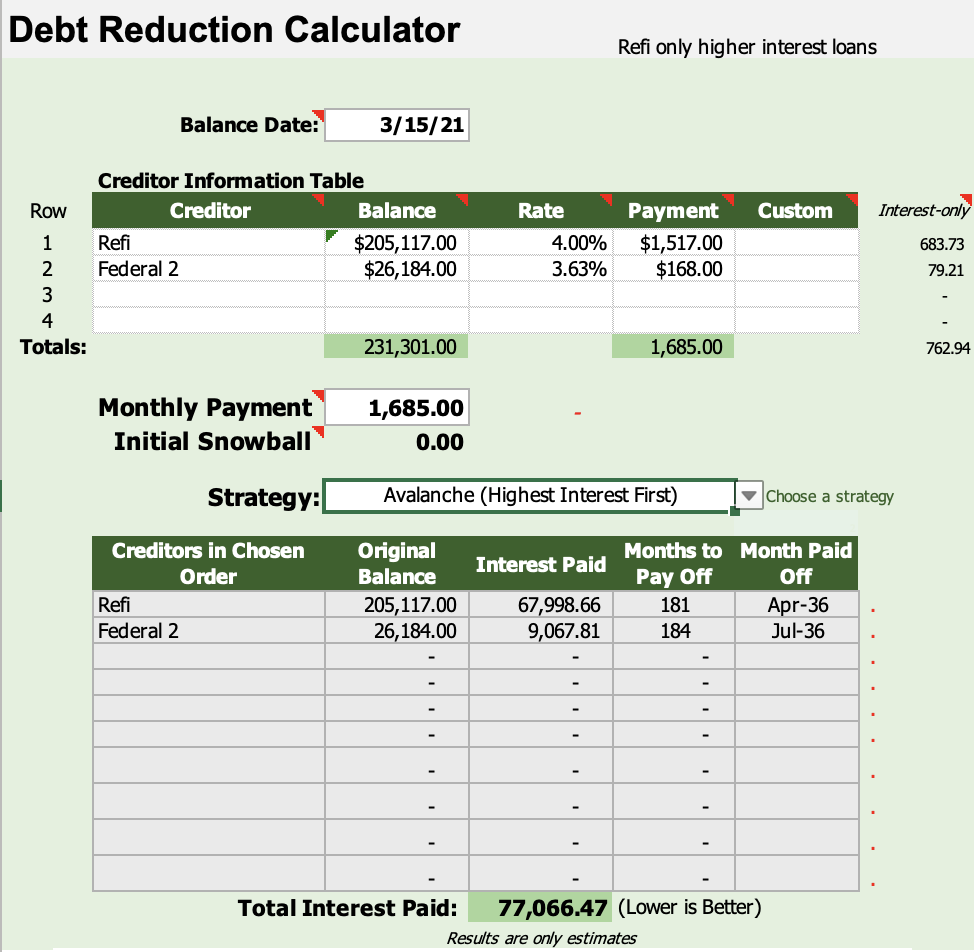

Definitely an improvement, saving them $10,724! But let’s take it a step further assuming that when the refinanced loan was paid off, they’d then snowball their normal payment ($1517) into the federal loans to pay those off faster:

A whopping $215 of savings, but shaved off a year and ½ of time! Hmm. So let’s take it another step further and look at if we just refinanced everything together at the 4% interest rate for a 15-year term from the beginning:

Refinancing everything from the beginning is more optimal! So in this case, I would suggest simplicity and refinance everything, even if we couldn't get lower than the lowest interest-rate loans.

A good rule of thumb to use here is finding the weighted average interest rate for the whole debt situation, which in this case is 4.5%. Here’s how to calculate this:

As long as a refi interest rate offer is lower than the weighted average, green light on refinancing everything together. If not, that’s when cherry-picking might make sense, leaving the lower interest rates out of the refinance and snowballing your payments as loans are paid off.

There’s obviously MANY ways to look at this but overall remember:

- If your federal loan repayment path is forgiveness, it does NOT make sense to refinance any part of your federal balance. This results in paying more than needed.

- Generally, if the refinance offer is a lower interest rate than the current weighted average interest rate of all of your loans, there’s not a big advantage to leaving the lowest interest loans out.

Want Help Solving Your Student Loans? We Can Help Figure Out the Best Path to Repayment

If you’ve made it through the whole article, kudos. Let our team save you a ton of time and probably a lot of money too and create a customized student loan plan for you.

Take a look at how our student loan consult service could save you thousands of dollars over the life of your loan payback.

Refinance student loans, get a bonus in 2025

| Lender Name | Lender | Offer | Learn more |

|---|---|---|---|

|

$500 Bonus

Bonus for eligible users who refinance $100k or more (bonus from SLP, not SoFi)

|

Fixed 4.49 - 9.99% APR

Variable 5.99 - 9.99% APR with all discounts with all discounts |

|

|

$1,000 Bonus

For 100k or more. $200 for 50k to $99,999

|

Fixed 4.35 - 10:49% APR

Variable 5.88 - 10.49% APR

|

|

|

$1,000 Bonus

For 100k or more. $300 for 50k to $99,999

|

Fixed 4.35 - 10.74% APPR

Variable 4.86 - 10.74% APR

|

|

|

$1,050 Bonus

For 100k+, $300 for 50k to 99k.

|

Fixed 4.99 - 8.90% APR

Variable 5.29 - 9.20% APR

|

|

|

$1,099 Bonus

For 150k+, $300 to $500 for 50k to 149k.

|

Fixed 4.88 - 8.44% APR

Variable 4.86 - 8.24% APR

|

|

|

$1,250 Bonus

For 100k+, $350 for 50k to 100k. $100 for 5k to 50k

|

Fixed 3.99 - 11.09% APR

Variable 4.31 - 12.05% APR with autopay with autopay |

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2025 on whether you should pursue PSLF, SAVE or another IDR plan, or refinancing (including the one lender we think could give you the best rate).