The FUTURE Act made it possible for a borrower to share their income automatically with their student loan servicer for the purposes of recertifying their income driven repayment (IDR). However, this requires an individual’s consent. The Department of Education has made it very easy to provide that consent, but you might realize that providing that consent was a mistake.

We’ll show you in this article how to revoke consent for the IRS Data Retrieval Tool (DRT) for student loans. We’ll also cover why you might want to do this.

Why would anyone want to revoke automatic income sharing from the IRS for student loans?

What are the big categories of borrowers who might want to revoke consent for IRS data sharing? We’ll cover some below.

Borrowers using alternative documentation of income

Maybe you live in a community property state and know that you can submit form 8958 to split your income evenly if you file taxes married filing separate.

If you earn more than your spouse, you are happy to provide tax returns as proof of income because that income is lower. You are under no obligation to share additional information, so you can simply provide IRS access and not worry. We call this the breadwinner loophole.

However, if you earn less than your spouse and live in a community property state like California, then you’d be concerned about using tax returns because your income would not be correctly reflected by your tax return.

So, a borrower in this situation would want to recertify manually without providing IRS access.

Borrowers with large families

It’s not yet clear how or whether the IRS will share family size information with the Department of Education.

Because the new exemption is 225% of income for the SAVE plan, you will want to make sure you get credit for as large of a family size as is legal.

If a married couple files taxes separately, there’s a chance the IRS might not give credit for all the children if you didn’t claim them. We don’t know this yet, but it might be safer to revoke consent if you’ve already given it until we know more.

Borrowers with privacy concerns

The most obvious reason to revoke consent for IRS data sharing would be a borrower’s desire for privacy.

You might have concerns over data breaches and hacks as well, but a borrower already must submit large amounts of personal data to fill out a FAFSA, so it’s unlikely that you’re putting yourself more at risk for providing consent for IRS data sharing to recertify IDR.

Revoking IRS consent is up to you

Lawmakers saw fit when writing the FUTURE Act to allow borrowers to have control over their data.

That means if you don’t fall into one of the categories above but want to revoke consent, you should feel free to do so.

Here are the steps on how to do this.

Steps for revoking authorization for the IRS Data Retrieval Tool

Follow the guide below to revoke access for the IRS data sharing if you’ve already approved it.

Step 1: Go to Settings

Once logged in to studentaid.gov, click on the drop-down where your name is and click “Settings.”

Step 2: Click on “Financial Information Access”

On the left-hand side, you’ll see “Financial Information Access.” Click that.

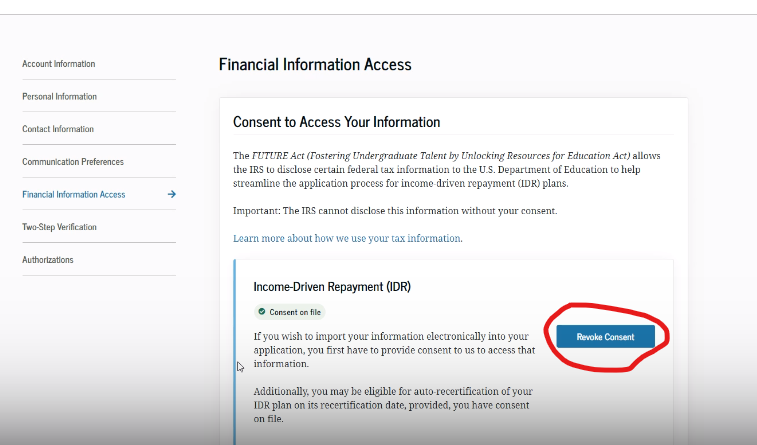

Step 3: Press the “Revoke Consent” button

If you’ve already provided access to the IRS Data Retrieval Tool, you’ll see a button to click “Revoke Consent.” Press that.

Step 4: Enter your name and press “Revoke Consent”

Enter your name as your digital signature, and then press the “Revoke” button again.

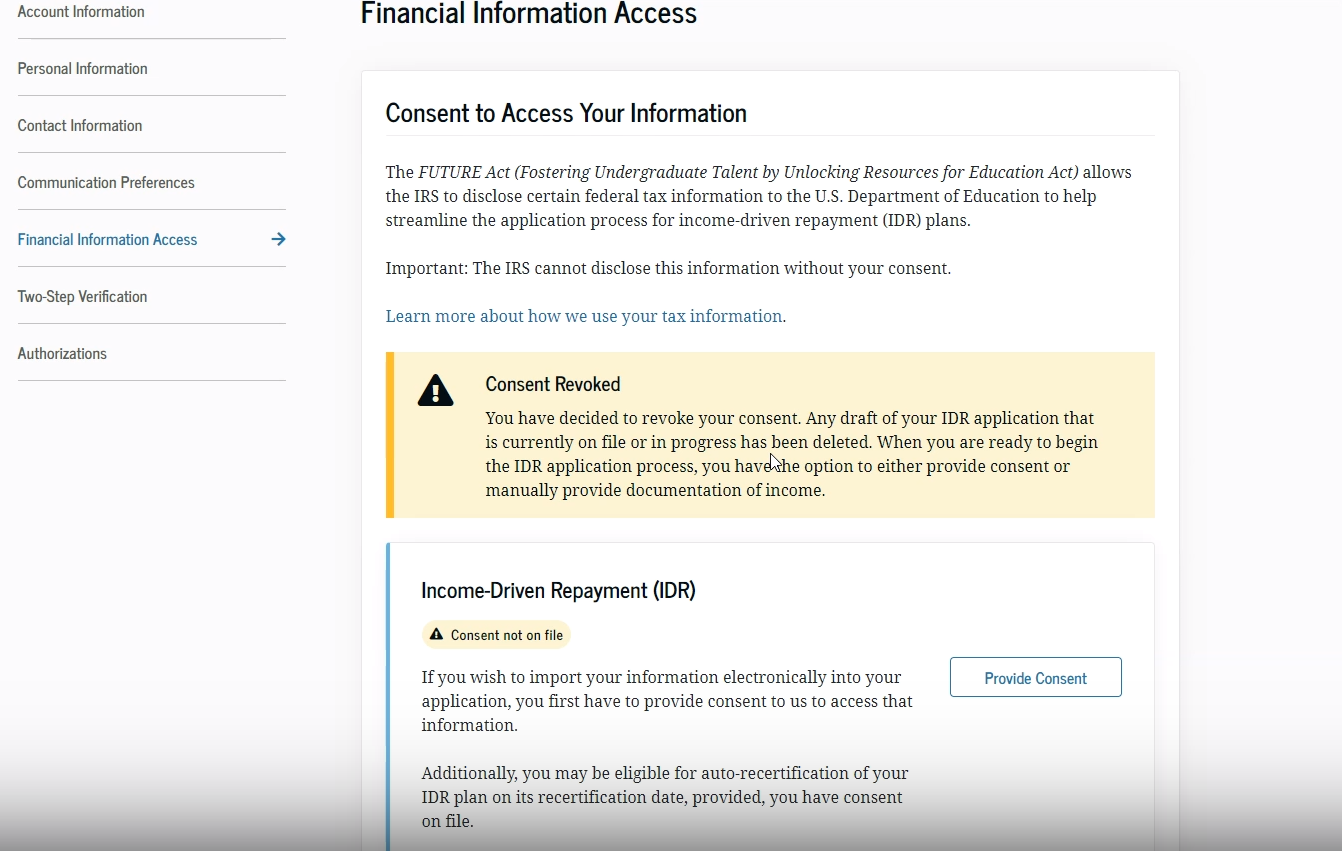

Step 5: Your consent is now revoked

You’ll see the following message below, and your IRS consent is now revoked.

Getting help to figure out whether you should provide IRS data sharing consent

It’s your choice whether or not to recertify your IDR automatically or manually.

In part, it’s a decision about privacy.

But most Gen Z, millennial, and Gen X borrowers won’t care as much about that as what the impacts are on your household financially.

We can help provide an independent view as to what’s best for your situation. Just book a consult with our experts to find out the best path for you in regards to IRS data sharing for IDR.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).