The SAVE plan has truly changed the math behind college loan repayment, particularly for undergraduate degree holders.

Being debt free has psychological advantages, but the math is undeniable that the average college graduate should pursue student loan forgiveness instead of debt repayment.

How the SAVE plan works for undergraduate degree holders

Under SAVE (which stands for Saving on a Valuable Education), borrowers with only undergraduate loans must pay 5% of their discretionary income.

Discretionary income on the SAVE plan means 225% of the federal poverty line based on your family size. If you file taxes married filing separately, you exclude your spouse from the family size calculation.

Here’s how much income you can earn as of 2024 before having to pay anything on the SAVE plan:

| Family size | Income limit |

|---|---|

| 1 | $33,885 |

| 2 | $45,990 |

| 3 | $58,095 |

| 4 | $70,200 |

| 5 | $82,305 |

| 6 | $94,410 |

You may have heard the average income for a college graduate is around $60,000 per year. If someone has a couple of children and files taxes separately, the deduction for a family size of three is almost large enough to ensure that person would pay $0 a month on the SAVE plan.

I’ll go into more rigorous detail in a bit, though.

So, the SAVE plan would first determine how much protected income a borrower should earn before taking anything.

Once a borrower earns more than the minimum protected income, the SAVE plan takes 5% of the amount above that level (if a borrower only has undergraduate loans).

If a borrower has both graduate and undergraduate loans, then the calculation would be a weighted average between 5% and 10%, depending on the relative percentage of grad vs. undergraduate debt.

Example of a SAVE plan payment calculation

We have a student loan repayment calculator that will do this for you but pretend you are a single teacher earning $50,000 per year with no children. You owe $30,000 of student debt from undergrad.

Your SAVE plan payment would be 5% * ($50,000 – $33,885) / 12 = $67 a month.

How the SAVE plan forgiveness timeline varies depending on your loan amount and job

The timeline for SAVE plan forgiveness for the following types of borrowers is just 10 years:

- Public servants.

- Borrowers with less than $12,000 of student debt originally borrowed.

For every $1,000 above $12,000 you owe, you add one year to your forgiveness timeline until you reach a maximum of 20 years.

For borrowers in the private sector with more than $22,000 of undergraduate debt, the timeline under SAVE is 20 years until forgiveness.

According to Matt Chingos at the Urban Institute, “Those with the lowest debt levels are least likely to have degrees.”

This means that a large number of borrowers would have to pay very little on their relatively small balances before these get forgiven in 10 to 20 years.

Higher-earning borrowers in the public sector would have an easier time getting forgiveness over a 10-year period instead of 20 years.

So, if a majority of borrowers earning an average wage in the private sector would be better off pursuing forgiveness over a 20 year period, this effectively proves the case that most college graduates with bachelor’s degrees should pursue forgiveness.

How the 10-year, 5% of income SAVE plan with PSLF makes loans much more forgivable

Under the old PAYE (Pay As You Earn) and IBR (Income Based Repayment) plans, the income deduction was just 150% of the poverty line. What this meant in practice is that even a modest income of $50,000 a year would result in $300 a month payments. That amount would entirely extinguish a typical $30,000 debt from undergrad.

Under the new SAVE plan with its larger protected income and 5% of income payment formula, the math is now much easier to receive forgiveness for public servants of any five-figure and low six-figure income level, even on a modest amount of debt.

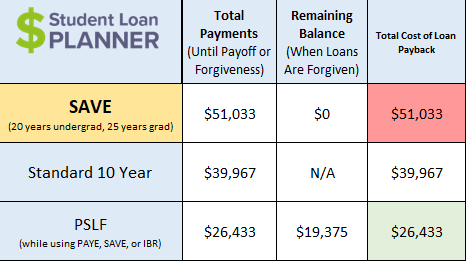

Consider the payments a nurse earning $80,000 a year with no children would make on the SAVE plan under PSLF over 10 years:

Without the SAVE plan, this nurse would not want to pursue forgiveness because she would pay the entire loan off before receiving any loan discharge.

The median annual earnings for a bachelor's degree holder is roughly $61,000, so $80,000 is substantially higher than the average.

Also, we’re assuming this individual had no children. If she had children along her repayment journey, this would significantly lower her payments under the new discretionary income definition that SAVE uses.

Why a typical private sector employed college graduate would choose 20-year SAVE plan student loan forgiveness

Again, remember that the average student debt is roughly $37,000. For a four year degree, that average is closer to $30,000.

As stated above, the median earnings of a college graduate are roughly $61,000.

In the first year after graduation, your prior year's income as a student is usually $0.

In the second year after graduation, your prior year's income usually encompasses only part of the calendar year (as most college graduates start their first job in the summer after graduation).

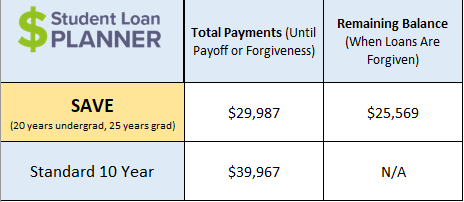

For that reason, we will run a simulation for a borrower with a $61,000 starting salary. Their first payment under SAVE is $0 a month because of the prior year student income being zero. We assume their second-year tax return shows half their stated income due to only working part of the year.

Every year after that, I assume a $61,000 salary that grows 5% a year. Keep in mind the median starting salary for a college graduate is lower than what I’m modeling, as this represents the median for graduates aged 25-34.

The average person has two children in the U.S.. Let’s assume this individual has one child five years after graduation. Here’s their payment results:

You might say, “Oh look! Almost $30,000 of payments on $30,000 of debt. This person should pay off their debt!”

But that ignores the cost of interest and the fact that inflation occurs over a 20-year period.

So, this above-average income individual with fewer children than average and an average level of undergrad-only student debt is better off pursuing forgiveness.

This is also before taking into account situations that vary based on the individual, such as being married to a spouse with a significantly lower income who would increase the discretionary income deduction or contributing some amount to a pretax retirement account.

Unique circumstances where a four-year college graduate could get forgiveness even with a six-figure income

Borrowers with a stay-at-home spouse in a community property state could split their income 50/50 and pay significantly less than the amount represented by their individual incomes.

Other situations where a borrower with six figures of income could get forgiveness even on a moderate amount of debt include having a larger than average family size, having significant pretax deductions such as maxed out 401k and HSA accounts, or unusually large business deductions such as Section 179A, real estate depreciation or short-term rental “losses.”

Many of these advanced planning cases would require calculating the cost of married filing separately for borrowers who are married.

See if you should pursue forgiveness on your debt

Whether you owe $10,000, $30,000 or $300,000, it’s important not to allow conventional wisdom to sway you on the correct loan repayment strategy.

Sometimes it’s truly the right call to pay back your debt. There are also plenty of situations where it’s a gray area, and a reasonable person could go either way.

But if you want to figure out how to optimize forgiveness or if forgiveness is right for you, check out the Student Loan Planner consult service.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2025 on whether you should pursue PSLF, SAVE or another IDR plan, or refinancing (including the one lender we think could give you the best rate).