This case study is a fascinating look into why the higher education system is broken in America. We will call this reader Jane to protect her anonymity. I'll describe her situation rather than quote what she told me. She has $388,000 in debt from a single, consolidated loan directly from the federal government at an interest rate of 6.75%.

Jane is a veterinarian who makes about $75,000 a year. She wants to buy a house, start a business, have a family, and a host of other things, but she is worried by her massive student loans. Jane feels trapped and unable to achieve anything financially with such a big yoke around her neck. The good news is that she has options. If massive student loans have got you down, there is hope. Here is her story and some ways her finances do not have to be controlled by the cost of her education.

WHAT DOES JANE'S BUDGET LOOK LIKE?

Jane currently contributes 4% to her 401k to get the employer match. She takes home about $49,000 and has expenses around $45,000. Her yearly cushion is $4,000. She also gets a bonus each year ranging from $3,000 to $6,000 depending on the performance of the private animal hospital where she works.

She spends $740 a month on her loans, or $8,880 a year. A little quick math shows that she is falling fall short of the interest payments alone on her massive student loans. If she only covered the interest payments, she would need to pay $26,190 annually, amounting to over 50% of her take home pay. If she paid enough to actually bring down the loan balance, her yearly payments would be over $30,000. The most she could ever expect to earn as a veterinarian is between $100,000 and $200,000 if she started her own business. She will never have enough money to pay off her massive student loans AND accomplish the other goals she has in life.

HOW DID JANE'S EDUCATION COST THIS MUCH MONEY?

Unbeknownst to me, veterinary school is unbelievably expensive. Just to get the education needed to practice costs a low six figure sum. Say she went to a middle-of-the-road, expensive undergrad college. She accumulates $100,000 in debt over the course of four years there. In grad school, she adds another $200,000. These loans grow at around 6% annually, and by the end of her program you end up with a loan balance of $388,000.

WHAT ARE JANE'S OPTIONS WITH A LOAN BALANCE LARGER THAN A MORTGAGE?

We have established that paying off her loans is not realistic, unless she lived an extreme lifestyle more in line with someone trying to achieve an extremely early retirement. I have written about the Public Service Loan Forgiveness Program (PSLF) in the past. She could work 10 years for a not-for-profit organization and have the balance forgiven tax-free. After speaking with Jane, there are not many jobs in veterinary medicine available in the public sector. You could work for the government or academia, but these jobs are few in number in veterinary medicine.

Jane mentioned that she makes payments on her massive student loans with the old Income Based Repayment plan (IBR). I wanted to see if she had other options. So, I performed an analysis on her loans to see if she had eligibility for other payment options. The federal government sponsors such plans as PAYE (Pay As You Earn), the new IBR, REPAYE (Revised Pay As You Earn), or Biden's new proposed income-based repayment plan. The first test we need to apply is whether or not she has eligibility for all three (potentially four) programs. To use the new IBR plan, you need to be a “new borrower.” I looked up the definition from the student loan website studentloans.gov.

You're a new borrower for the IBR Plan if (1) you have no outstanding balance on a Direct Loan or FFEL Program loan as of July 1, 2014 or (2) have no outstanding balance on a Direct Loan or FFEL Program loan when you obtain a new loan on or after July 1, 2014.

Jane does not qualify on either count, so new IBR is out. She had loans outstanding before 2014. She also had massive student loans already when she consolidated her loan in late 2014. What about the PAYE program? Is she eligible for that one?

You're a new borrower for the PAYE Plan if (1) you have no outstanding balance on a

Direct Loan or FFEL program loan as of October 1, 2007 or have no outstanding balance on a Direct Loan or FFEL program loan when you obtain a new loan on or after October 1, 2007, and (2) you receive a disbursement of a Direct Subsidized Loan, Direct Unsubsidized Loan, or student Direct PLUS Loan on or after October 1, 2011, or receive a Direct Consolidation Loan based on an application received on or after October 1, 2011.

Unfortunately, since Jane was an undergraduate in Fall 2007, she had a loan disbursement just before October 2007, and she is thus ineligible for PAYE.

The REPAYE program and the old IBR program are available to everyone regardless of their loan status. These are the two choices we have available. It would obviously have been better if we could have considered the PAYE program, but we are stuck with these two options, since Jane cannot afford the standard 10 year repayment schedule.

IBR VERSUS REPAYE

This is not meant to be an exhaustive guide to student loans. We are just looking at Jane's situation here. We have to take a look at the old IBR program and compare it to the REPAYE program for her specific situation. To figure out which plan is better for her, I spoke with Jane about very personal topics. I needed to know if she planned on marrying one day, how much she expects her income to grow in the future, and how much of a gambler she is. All of these answers determine which program to choose.

The old Income Based Repayment plan limits payments to 15% of discretionary income. Because her massive student loans have such a high monthly payment under a traditional 10 year payoff plan, she should always qualify for financial hardship to limit payments to a percentage of her income. These two programs treat spousal income differently, which is why I needed to know her marriage plans. If she married a very high income spouse, you can exclude that income from IBR by filing taxes separately. However in the REPAYE program, you must include your spouse's income in the student loan payment calculation no matter what. Since she plans on marrying, we have one point for IBR.

To the question about her future income prospects, she felt like growth was limited. If she starts her own business it might grow into the low 100s, but certainly not mid-six figures or anything. REPAYE does not cap payments. It costs 10% of discretionary income no matter how high that income is. So since she believes she will have limited salary growth in the future, this is a point for the REPAYE program. She also mentioned that she did not believe she would be marrying a high income partner, so that is another point for REPAYE, as her spouse's future income would have limited impact on her payments. REPAYE also costs 10% of income instead of 15%. So, until she gets married, REPAYE will lower her monthly payment significantly.

Perhaps the most pressing consideration in deciding between REPAYE and IBR is the accumulation of accrued interest. The REPAYE program has an incredible feature in this regard. If your payments are not sufficient to cover the interest payments under REPAYE, the government pays for 50% of this interest. That is an incredible benefit for low income borrowers with large debt loads. If she ever leaves the REPAYE program, this interest gets added onto her debt. The government used to reserve this interest subsidy for subsidized loans only, and then only for the first few years of borrowing. The REPAYE interest subsidy is for the life of her loan. The only way to see how good this benefit could be is to run some numbers. This simulation will require a lot of assumptions.

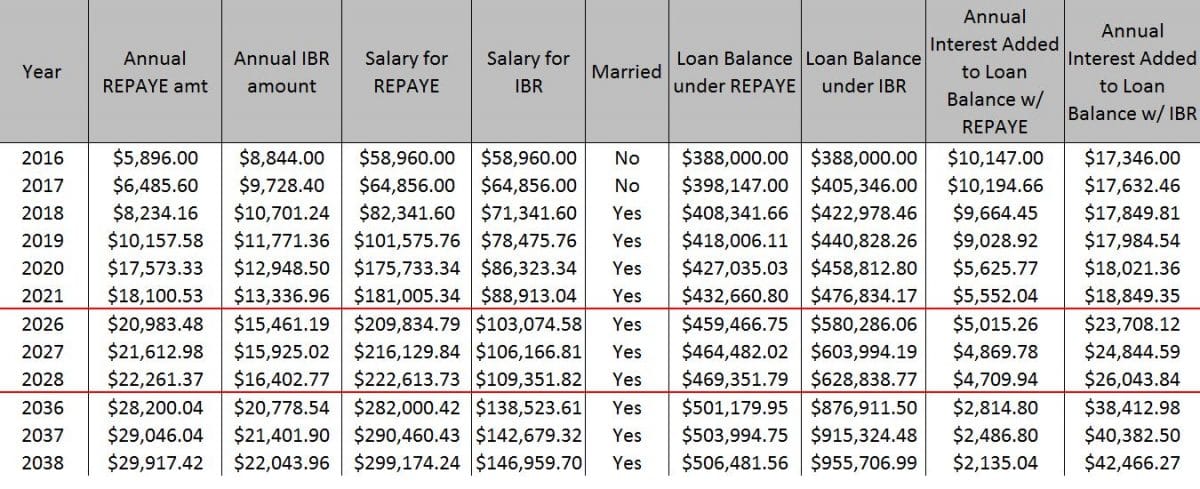

- Jane started making payments on her direct consolidated loan from the federal government in 2014. Because the balance is so large relative to her current and future expected income, I'm assuming the feds forgive the loans in 2038 after 23 more years.

- I assume Jane's salary starts at $75,000 and grows by 10% over the next 5 years, after which point I assume it grows at 3% a year.

- I assume she marries in three years. Her current boyfriend is in grad school to become a professor, so I assume he makes an income of $20,000 until 2020, when he makes $75,000 a year. I grow his salary at the rate of inflation too.

THE SIMULATION RESULTS FOR HER MASSIVE STUDENT LOANS

Notice that REPAYE payments are lower. That is, until you include her husband's income in the IBR payment calculation in 2020. The salary under each program is lower than what she makes. The federal government excludes a portion of salary equal to the federal poverty line.

Check out the two columns on the right. This column shows the unpaid interest on her loans added to the total balance after each year. After 23 years of payments, she is still not able to make only the interest payments under either plan. However, under the REPAYE program, the interest subsidy kicks in and prevents some of it from adding to the loan each year. Because of this feature, her massive student loans grow to just over $500,000 instead of almost $1,000,000 over this time period.

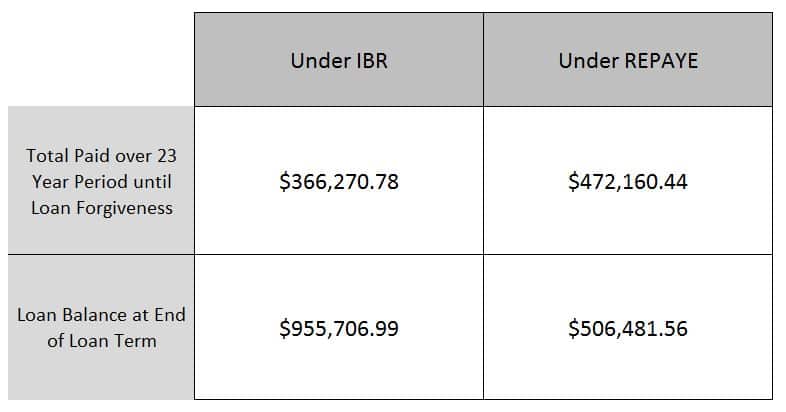

This summary chart above shows how much she would pay under each of the two plans with the assumptions I mentioned. The REPAYE program will definitely result in her paying more if her spouse works. However, The loan balance is tremendously smaller with REPAYE. Now the final question.

THE GAMBLE

In 23 years, she will have made a total of 25 years' worth of payments on her massive student loans that originated in 2014. Because she has a single, direct consolidation loan from the federal government, she would then be eligible for forgiveness. The gamble is that currently this forgiveness is considered taxable income! That means if she goes with IBR, in 23 years she will have to pay federal, state, and local income taxes on a million dollars. In New Jersey where she lives, that could cost more than $500,000. So much for forgiveness. In contrast, if she had a nonprofit job and qualified for the Public Service Loan Forgiveness program, the government would forgive the entire amount tax free after 10 years. This is a huge discrepancy between working at a not-for-profit employer and a for-profit employer.

I would argue that the current state of loan forgiveness, especially for massive student loans, is unfair. If you want to encourage people financially to work for not-for-profit hospitals, the government, charitable organizations and the like, fine. But don't make for-profit forgiveness taxable and nonprofit forgiveness tax-free! There should either be no forgiveness or the programs should mirror each other. Congress did not want to account for the billions they added to the federal budget deficit with this bill. That's why I think they passed what they eventually want in a piecemeal approach.

How could citizens who do not have enough money to make their standard 10 year student loan repayments come up with hundreds of thousands of dollars in taxes without declaring bankruptcy? This law is absurd. I fully expect something to change between now and when Jane qualifies to have her loan balance forgiven.

That said, I do not have a crystal ball. If the feds leave the current rules in place, REPAYE is the better plan. She will pay about $100,000 more over 23 years, but she will save about $200,000 in taxes in 23 years compared with IBR. The large tax payment could even bankrupt her if she did not plan for it years ahead of time. She could lose her house, her car, and her business. The IRS would probably work with her and put her on a payment plan. With the REPAYE program's interest rate subsidy, REPAYE is the safer option.

Worst case scenario she pays about $100,000 more in payments. In that case, Congress would have passed a law making all student loan forgiveness tax-free. Hence, she would not have to pay about $200,000 in tax payments. Best case scenario, the government keeps the rules as is. She would save $100,000-$200,000 after subtracting the extra money she paid into the program from the higher tax bill. With REPAYE, she eliminates the uncertainty of a $500,000 tax payment when the government forgives the loans in 23 years. With REPAYE, the largest tax payment she could owe is around $250,000.

If I was in Jane's shoes, I would want to eliminate the uncertainty of bankruptcy in 23 years because of massive student loans. I would use the REPAYE program, making sure to re-enroll each year as the program requires. Once she chooses REPAYE, she needs to stay in the program, or the interest becomes capitalized. She could chance that Congress changes the rules over the next two decades to save $100,000. If she is wrong, the large tax bill would be very painful financially.

MASSIVE STUDENT LOANS DO NOT HAVE TO BE A FINANCIAL BURDEN

I love this analysis I did for Jane, because it gave her hope that she has a financial future. Universities are more dishonest than credit card companies sometimes. They jack up the cost of tuition to unreasonable levels. They fail to explain the unbelievable financial strain that will stay with graduates for decades. No matter your balance, I hope this case study shows that you can conquer massive student loans.

I Can Help Figure Out Your Student Loans

For a similar, personalized analysis, contact me by clicking on the button below. I only charge a one time fee to analyze the data in order to suggest the best student loan repayment plan for you. On the low end, I might be able to save you a few thousand dollars. On the high end, I could save you hundreds of thousands of dollars.

What do you think about federal student loan forgiveness and repayment programs? Should they change? What has your student loan journey been like? Comment below!

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).