Recertification time for federal student loan borrowers on an income-driven repayment (IDR) plan can stir up some anxiety. Many borrowers don't know how to recertify an income-driven repayment plan. So, it's common to worry about whether your payment will increase or not. Additionally, major milestones, like getting married or having children, can significantly impact your payment.

This guide will break down frequently asked questions and help you feel more confident when you complete this reporting requirement.

How to recertify income-driven repayment: 3 Tips for filling out your IDR Plan Request Form

First things first, let’s cover some basics, such as when to recertify, how your income is used to calculate your payment, and simple ways to lower that payment over time.

The video below covers the bulk of what you need to know for the recertification process. Note updates have been made by the Department of Education since this tutorial was recorded. The layout may look a little different, but the process, key decision points, and trigger questions you’ll see throughout the application are still the same — so this walkthrough will still answer most of the questions borrowers run into.

1. When to recertify for income-driven repayment

You can submit an income-driven repayment (IDR) plan request form at any time. However, you’re only required to submit updated information once per year on your IDR anniversary date. If your income has dropped, for example, it's a great time to consider completing a new application ahead of your anniversary date. This will immediately recalculate your monthly payment amount because your payment is no longer reflective of your current income.

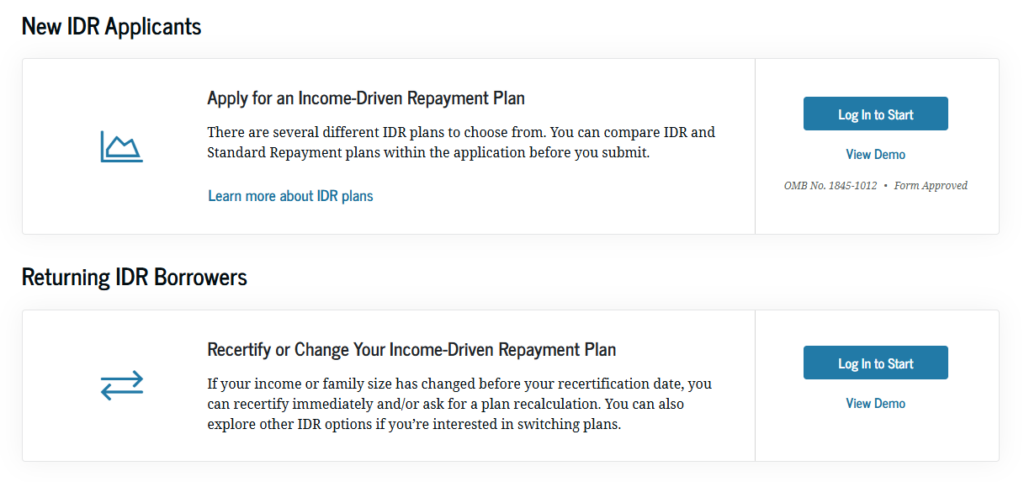

Take note of the different application purposes and apply accordingly:

- New IDR Applicants: This is for those who are not currently on an income-driven plan and want to apply.

- Returning IDR Borrowers: Select this option if you're 1) already on an income-driven repayment plan and you need to recertify your income, 2) if your income or family size has changed prior to your required recertification date and you want to recalculate your payment, or 3) you want to explore other IDR options because you’re interested in switching plans.

2. How your adjusted gross income factors into your IDR plan

The IDR Plan Request form will always link back (or try to link back) to your most recent federal income tax return to collect your adjusted gross income. If the IRS data retrieval tool does not successfully link to your last tax return, it could be because:

- Your name and/or address were not exactly how they appeared on your last tax return (e.g., putting “Sam” for your first name if your return said “Samantha”).

- The IRS website might be offline or experiencing some other technical issues.

- Your tax information might not be available (for instance, if you filed your taxes electronically within the last three weeks or via postal mail within the last 11 weeks).

- Your federal tax return indicated an outstanding balance owed, which may result in a delay in processing.

You're required to submit alternative documentation of your income (e.g., a paystub, employer letter certifying gross income, etc.) if your tax return doesn't link through. The same applies if you answer “Yes” to the question about whether your income has significantly decreased (e.g., you lost your job or experienced a drop in income) since you filed your last income tax return.

You can get repayment estimates using the StudentAid.gov loan simulator. However, it can't predict your future payments with 100% accuracy due to general assumptions that must be made. For example, it will assume the family size and income growth percentage you enter will remain the same for every year. Want some extra help? Schedule a consultation here to get your customized student loan plan.

3. How to reduce your AGI

Because your payment is based on AGI, lowering your AGI can lower your payments. A simple way to reduce your AGi is by saving in your pretax accounts. This includes a 401(k) or 403(b) retirement account, individual retirement account or health savings account. The maximum allowed in your employer retirement plan is $24,500 for the year 2026. Contributing to pretax accounts reduces your AGI, which reduces your student loan payments while building your long-term wealth.

FAQs about how to recertify an income-driven repayment plan

Here are answers to some of the most common question we get from borrowers looking to recertify their income.

How does “family size” factor into my payment calculation?

Family size matters for your IDR plan because it’s part of your federal student loan repayment calculation. Your payment is based on discretionary income, which factors in the poverty line for your household size.

You count as one household member. If you have a spouse, you have a household size of two. The application will automatically count you (and your spouse, if applicable). The application will also ask how many children you claim as dependents on your tax return to include in your family size.

What if I lie on the application about my family size or dependents to reduce my payment?

Don’t lie. Any person who knowingly makes a false statement or misrepresentation on this form can be subject to penalties. This may include fines, imprisonment or both.

What if I got married this year, but we haven’t filed taxes together yet?

Under marital status, you must disclose that you’re married (unless you’re not legally). If you indicate you're married, you'll get the poverty line deduction for a two-person household size.

It will then use the IRS data retrieval tool to link back to your most recently filed tax return, which should be for a single filer.

The next questions will trigger whether or not to ask for your new spouse’s income information to be included in your payment calculation. If you didn't have access to your spouse’s last tax return since you weren’t married yet, select “no”. The application will continue to be based on just your own income (your last tax return as a single filer) for the next recertification period.

What if both my spouse and I have federal student loan debt?

If you both have federal student loan debt, your payments will affect each other. Filing taxes jointly will look at your debt load as household debt and a household monthly payment calculation. It will proportionally split that household payment between you two. Therefore, the spouse with more debt will have the larger payment.

If you both have federal student loan debt and file taxes separately, it will continue to keep your payments off of your own income and not look at your debt as a household.

What if my last filed tax return was filed jointly with my spouse?

Your payment will be based on that joint AGI, even if you want to exclude your spouse's income. This is the case unless you're separated from your spouse and unable to access their income information.

You can submit alternative documentation if your income has decreased since the last tax return by answering the question, “Has your income significantly decreased since you filed your last federal income tax return? For example, have you lost your job or experienced a drop in income?” However, alternative documentation from your spouse will still be required.

If you don’t want your spouse's income factored into your payment, you must file taxes separately on your next tax filing.

How long does a payment, based on the current recertification period, stay the same?

Your payment based on your recertification stays the same for 12 months. Your servicer will notify you to submit recertification again a month or two out from your annual deadline. Completing the annual recertification early does not change your payment early, and your new payment won't apply until your previous payment schedule ends. However, you can recalculate your payment early if your income has decreased.

What happens if I don’t recertify?

If you don’t recertify, your payment will switch to the 10-Year Standard Repayment Plan, causing your payment to more than likely go up. Your unpaid interest may be capitalized, meaning it will be added to the principal balance of your loans.

Knowing how to recertify your income-driven repayment plan puts you in the driver's seat

Recertification certainly adds to the high-maintenance component of federal student loans. However, you can stay on top of your IDR plan by feeling more confident in the questions being asked during this application process and knowing what responses trigger follow-up questions.

If you’re unsure of the best student loan repayment strategy for you and your family or need help figuring out how or when to recertify your income-driven repayment plan, the team at Student Loan Planner® would love to help you. We’ll review your whole student loan situation to help create the best plan for paying your student loans off or having your debt forgiven.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.