Obstetricians and gynecologists, commonly called OB/GYNs, treat women throughout life with an emphasis on the reproductive system. Gynecologists work to maintain patients’ reproductive health and monitor issues specific to females, while obstetricians focus on guiding women through pregnancy and childbirth.

Although an essential profession, pursuing an OB/GYN career comes at a steep cost. After earning an undergraduate degree, you’ll toil through four rigorous years of medical school followed by another four years of residency.

If you’re an OB/GYN or still in residency, you’re probably looking at a hefty six-figure student debt to repay. Student loan refinancing for gynecologists and obstetricians is a valid option for some who have private loans or are in private practice.

According to the Association of American Medical Colleges (AAMC), the average medical school debt totaled $200,000 in 2019, with 73% of graduates reporting debt. Its data found that for public-school attendees, the average cost was $250,222 and jumped to $330,180 for those who graduated from private medical schools.

Although obstetrician-gynecologists tend to earn high salaries, it’s still not easy to pay off student debt after getting certified as an OB/GYN. After all, your loans might total much more than the average AAMC figures.

If you’re struggling under a massive student loan debt balance, you can explore tactics for paying down debt more efficiently. Under the right circumstances, student loan refinancing for obstetricians and gynecologists significantly reduce your total interest charges and the time it takes to pay off your loans.

Let’s discuss the main criteria for deciding if student loan refinancing is the best choice for you and your medical student loan debt.

Average debt vs. salary for OB/GYNs

The $200,000 figure of median student loan debt for medical school graduates includes both undergraduate and medical-school debt. Keep in mind that’s an average of student debt for all medical professions, not specific to obstetricians.

If you pursue further specialization through a fellowship in a narrower field like reproductive endocrinology or gynecologic oncology, that usually means several more years of training that may delay your loan repayment timeline.

Obstetrician/gynecologists earn a median annual income of $233,610, according to 2019 Bureau of Labor Statistics data. Plus, the Medscape Physician Compensation Report for 2020 noted that OB/GYNs could also expect annual bonuses of an average of $44,000. That’s not quite as high as bonuses for other specialties like orthopedics ($96,000) or cardiology ($63,000), but it’s something to consider.

The same Medscape data showed physicians’ satisfaction with their income. Just over half (51%) claimed to believe their compensation level was fair.

Certainly, there’s a wide range for income and bonuses. However, if your OB/GYN salary is on the lower end of the scale and your debt is on the higher end, you’ll want to figure out ways to narrow that gap.

Related: How to Find Disability Insurance for OB/GYN Physicians

Most financially rewarding states for OB/GYNs

When making employment decisions as an OB/GYN, look at multiple financial factors: salary, employment benefits, malpractice premiums and the average cost of living in different areas.

States with the best salaries for OB/GYNs

Annual salary is a key factor in choosing employment as an obstetrician. The Bureau of Labor Statistics showed that Iowa was the highest-paying state for OB/GYNs, with an annual median salary of $283,280.

Other states that round out the top five for annual salary of obstetricians and gynecologists are Wyoming, Hawaii, Alaska and Alabama. Of course, if you’re seriously considering a move, you’ll need to examine the financial details of specific jobs to determine your best options.

Medical malpractice premiums in different states

Medical malpractice premiums can seriously impact your take-home pay and debt repayment ability. When you live in a region with higher-than-average costs, that reduces the amount of income you can earmark for debt payoff.

For obstetricians and gynecologists, the frequency of malpractice claims is higher than other specialties. Medscape’s 2019 Malpractice Report revealed that 83% of OB/GYNs had been named in malpractice lawsuits, tying the profession for third-place (with otolaryngology).

The five states with the lowest average medical malpractice premiums are Michigan, Rhode Island, Louisiana, Nebraska and Minnesota. Michigan’s average malpractice premiums are the best for physicians at $5,471 per year.

On the other end of the spectrum, obstetricians and gynecologists pay some of the highest medical malpractice premiums in Illinois, Montana, Wyoming and New York. In New York State, physicians pay over $16,000 annually (triple the rates in Michigan).

If you have some choice in where you choose to live and practice medicine, keeping this in mind can help you direct income efficiently toward paying student debt. Although relocation isn’t always an option, it’s one strategy with a potentially big payoff.

Student loan refinancing for obstetricians

Student loan refinancing for obstetricians may be a valid option for helping you pay off medical school debt. However, refinancing medical school loans is most advantageous only when loan forgiveness and other options are unavailable.

Student Loan Planner® estimates that refinancing medical school loans is the best option for a fairly small percentage of physicians (about 20% to 30%).

In general, obstetricians shouldn’t refinance if they have federal student loans and work for a public employer. Federal student loans provide borrowers with benefits such as eligibility for loan forgiveness and extended forbearance on payments in the event of hardship.

If loan forgiveness is at all a possibility, skip student loan refinancing for OB/GYN loans and keep that option open.

However, if you’re an OB/GYN in private practice and have private student loans, you won’t run the risk of losing federal benefits. Since private loans are ineligible for forgiveness programs like PSLF, student loan refinancing for gynecologists and obstetricians is wise.

How student loan refinancing for OB/GYN loans saves money

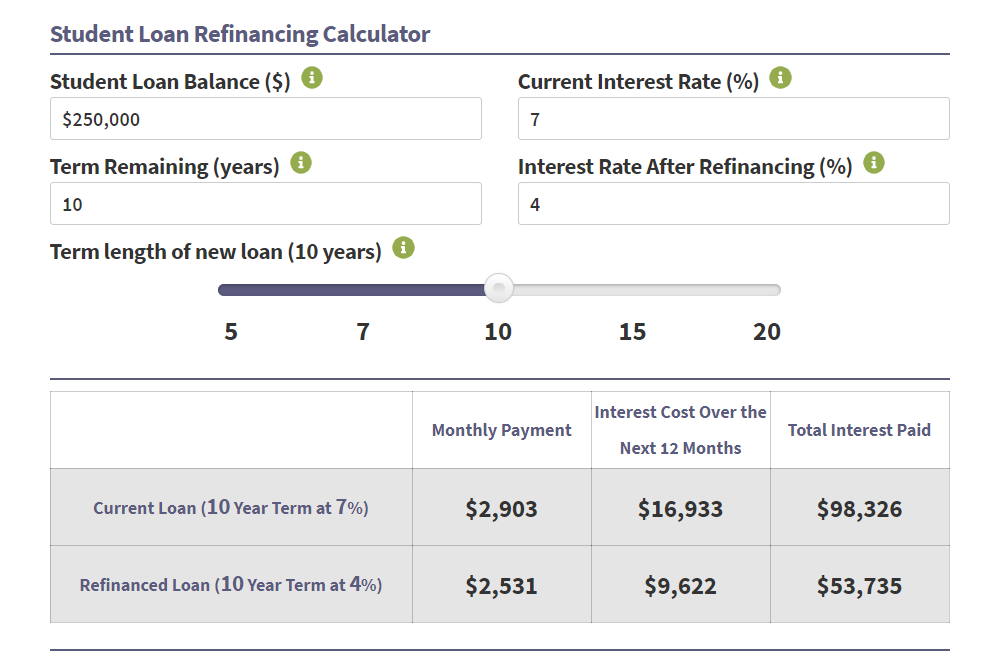

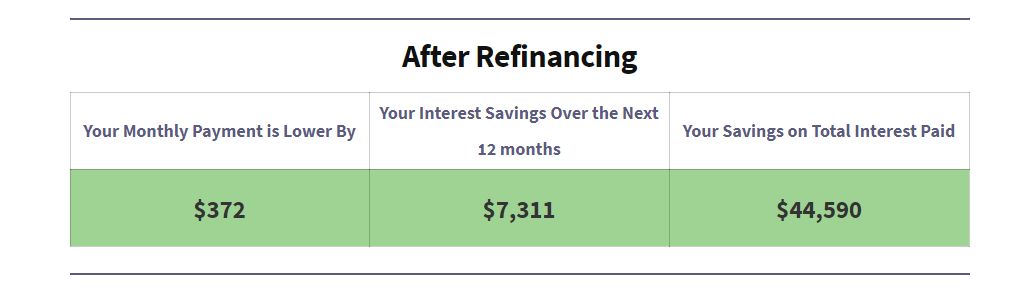

Let’s take an example of an obstetrician with $250,000 in medical school loans that aren’t eligible for forgiveness. If they currently pay a 7% interest rate and have 10 years of repayment remaining, their monthly payment is $2,903.

Drop these figures into the Student Loan Planner® Refinancing Calculator to see how they change. By refinancing to a 4% rate, the monthly payment drops to $2,531, saving $372 per month.

In that refinance scenario, the borrower would save a grand total of $44,590 in interest, dropping the total interest paid from $98,326 to $53,735.

Student Loan Planner® recommends KeyBank for refinancing medical student loans, since it offers reduced rates for physicians. When you refinance through Student Loan Planner®, you can receive a cash-back bonus up to $1,050.

If you’d like to compare more lenders, peruse our list of best banks to refinance student loans.

When student loan forgiveness might be a better route

For many physicians, refinancing doesn’t make the most financial sense. If you’re employed at a public hospital or other public practice and you have federal loans, you might qualify for student loan forgiveness.

Public Service Loan Forgiveness (PSLF) is a great tool for OB/GYNs working in the public or nonprofit sector. An income-driven repayment (IDR) plan that forgives your remaining loan balance after a certain number of years might also be an option.

Debt repayment strategies for obstetricians and gynecologists

If you’re an obstetrician or gynecologist early in your career or residency, you might benefit by combining debt repayment strategies. For example, you can enroll in an Income-Based Repayment (IBR), Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE) program while earning a lower salary.

These programs reduce loan repayment minimums temporarily, helping you manage other financial obligations. Following a job change resulting in a higher salary, student loan refinancing becomes more appealing because you can pay off debt more aggressively.

Get expert help before refinancing OB/GYN debt

For assistance with specific student loan refinancing for obstetricians and gynecologists, speak to a trained Student Loan Planner® consultant. They’ll thoroughly review and analyze your student loan debt to help you chart the best course of action.

Refinance student loans, get a bonus in 2026

| Lender Name | Lender | Offer | Learn more |

|---|---|---|---|

|

$1,000 Bonus

Bonus for eligible users who refinance $200k or more. $500 for $100k to $200k (bonus from SLP, not SoFi. Terms apply.)

|

Fixed 3.99 - 9.99% APR

Variable 5.74 - 9.99% APR with all discounts with all discounts |

|

|

$1,500 Bonus

For $200k or more. $1,000 for $100k to $200k. $200 for 50k to $100k

|

Fixed 3.74 - 9.99% APR

Variable 5.73 - 9.99% APR

|

|

|

$1,750 Bonus

For $200k+. $1,250 for $100k to $199k. $350 for $50k to $99k. $100 for $5k to $50k

|

Fixed 3.99 - 10.35% APR

Variable 3.63 - 10.72% APR with autopay with autopay |

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).