Partial Financial Hardship is a term associated with eligibility for the income-driven repayment (IDR) plans, Pay As You Earn (PAYE) and Income-Based Repayment (IBR).

It sounds aggressive, but having a partial financial hardship simply means that the payment calculated from your discretionary income must be lower than what your payment would’ve been on the Standard 10-year repayment plan.

What is a partial financial hardship?

Here's the technical definition from StudentAid.gov:

“Partial financial hardship is an eligibility requirement under the Income-Based Repayment (IBR) and Pay As You Earn Repayment (PAYE) plans. It is a circumstance in which the annual amount due on your eligible loans, as calculated under a 10-year Standard Repayment Plan, exceeds 15 percent (for IBR) or 10 percent (for Pay As You Earn) of the difference between your adjusted gross income (AGI) and 150 percent of the poverty line for your family size in the state where you live.”

You must have a partial financial hardship to be accepted into PAYE or IBR initially, but you can’t be “kicked off” the plan if your income gets to a point where you no longer have a partial financial hardship later on.

What would happen is your payment would cap-out or stop at that Standard 10-year amount, and that’ll be your payment going forward unless income decreases in the future. REPAYE on the other hand, doesn’t require a financial hardship so your payment has no cap under this plan as your income increases overtime.

Here are a few frequently asked questions when it comes to partial financial hardship.

What if I don’t have a partial financial hardship when applying for PAYE or IBR?

When you apply for an income-driven repayment plan, the application links back to your most recently filed tax return to verify income unless your current income is lower than what’s reflected on that last tax return. If it’s lower, alternative documentation is required such as a paystub or an offer letter to calculate your IDR payment.

If you don’t have a partial financial hardship when you apply for PAYE or IBR, your application will be denied and your loan servicer will place you on an IDR plan with the lowest monthly payment amount. REPAYE could likely be this next option because the only eligibility requirement for REPAYE is having Direct Loans.

What happens if I’m on PAYE or IBR and no longer have a partial financial hardship?

Once you’re already on PAYE or IBR (or any income-driven plan for that matter), every 12 months you have to update your income. This process is called IDR recertification. If your recertification generates a payment that exceeds the Standard-year repayment amount next time you recertify, your payment will cap-out at that amount.

You’ll get a notice from your servicer that says you no longer qualify for your income-driven repayment plan since you no longer have a partial financial hardship, BUT it can’t kick you off of the plan like I mentioned before.

The letter might make you think you need to switch repayment plans, but the reality is you don’t have to, and the servicer can’t make you either.

Why would I stay on IBR or PAYE after hitting the payment cap?

I can think of two reasons you’d want to stay on IBR or PAYE, and they both have to do with loan forgiveness.

1. Public Service Loan forgiveness (PSLF) is the biggest reason

The Standard 10-year payment, or in this case — your payment cap due to no longer having a partial financial hardship — still counts toward the 120 payments for PSLF.

Leveraging the payment cap can be a more efficient way to pursue Public Service Loan Forgiveness since it keeps the payment from increasing past a certain point. The result is that you’ll get to forgiveness paying less money toward your debt.

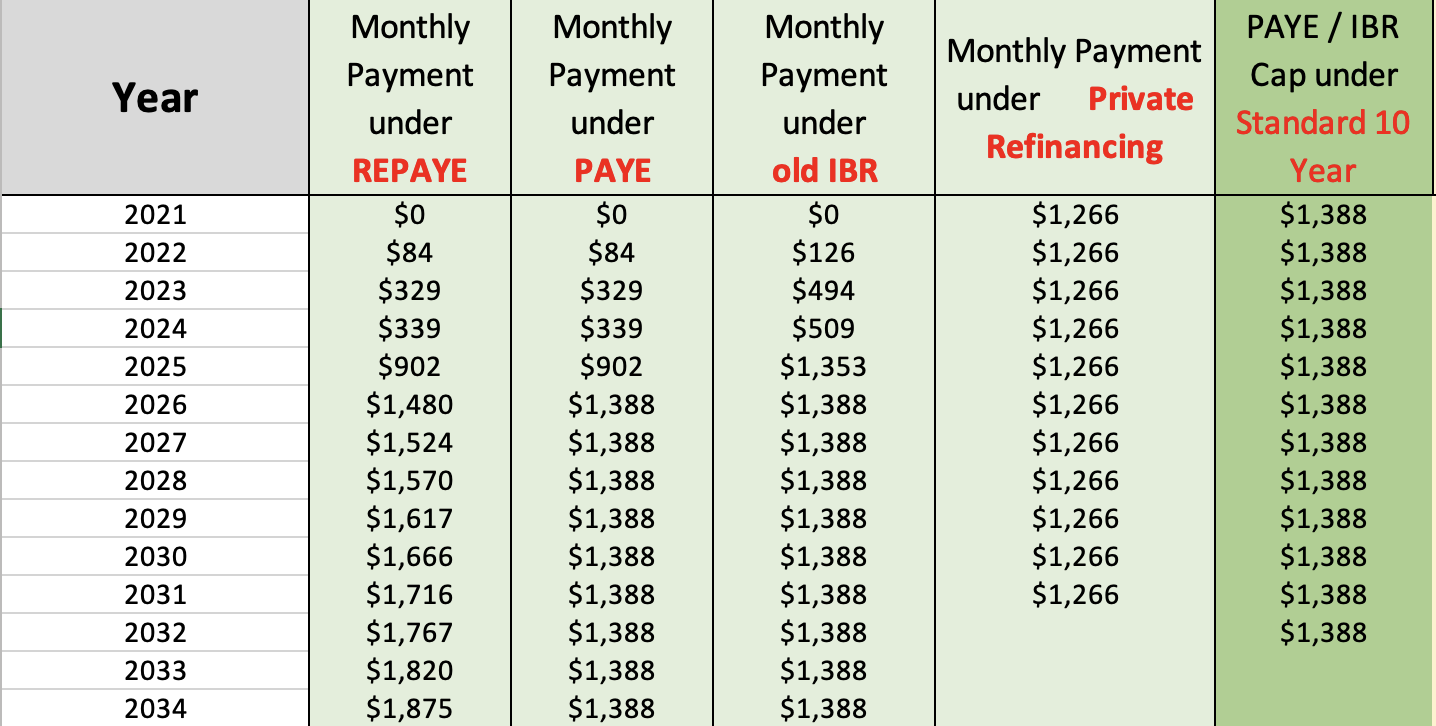

See an example below of a new-graduate physician who’s unmarried with $125,000 of student debt and their AGI from their tax return prior to graduation was $0. This physician has four years of residency with income at about $60,000 per year. Afterward, their attending annual salary will be $200,000, all while working in a 501(c)(3) hospital setting that’s PSLF eligible.

When pursuing forgiveness, the goal is to pay as little as possible to maximize how much debt is forgiven. PAYE and REPAYE are the least-expensive repayment plans, both based on 10% of discretionary income, but REPAYE doesn’t have the partial financial hardship requirement (i.e. payment cap).

This physician is eligible for PAYE now, because based on their most recent tax return on file, they meet the definition of having a partial financial requirement. Their payment’s less than their standard 10-year payment cap of $1388 per month. Their first 12 months of payments will actually be $0 per month (which still counts toward forgiveness).

You’ll see in 2026, the physician’s attending salary makes their payment higher than what the payment would’ve been if they’d started repayment from the beginning on the standard 10-year plan. That payment stops at $1,388 on PAYE, while REPAYE continues to increase with income growth.

This makes PAYE the optimal repayment plan to pursue PSLF.

2. Taxable loan forgiveness

Same story as PSLF for taxable loan forgiveness — you want to pay as little as possible to maximize how much you can get forgiven.

A payment cap can be handy in the later years of the maximum repayment period to keep your IDR payment as low as possible until forgiveness is achieved.

Let’s say forgiveness isn’t your primary goal. Another possible reason to stay on PAYE or IBR, without having a partial financial hardship, is that the payment cap could offer a payment ceiling for cash flow purposes.

If you didn't want the payment to keep increasing with income, but weren’t ready to commit to student loan refinancing yet, that payment cap could give you some peace of mind that the payment won’t go above a certain amount.

How do I find my standard 10-year payment amount?

This payment amount’s based on when you first entered the IDR plan. If you know approximately what your balance was at that time, take the 10-year amortized schedule of that balance to find your standard payment. Our student loan payoff calculator can do that for you, too.

You could also inquire with your servicer about what your payment cap is for PAYE or IBR. You might have to ask a few different ways to get the right answer. Here’s some suggestions:

“What’s the most my payment could be on PAYE or IBR?”

“What’s my standard 10-year repayment monthly payment?”

“What does my payment amount have to be under to be eligible for PAYE or IBR?”

“For me to have a partial financial hardship for PAYE or IBR, what does my payment need to be under?”

Can you switch to PAYE or IBR if you’re on REPAYE?

Yes, as long as you currently have a partial financial hardship, you can switch from REPAYE to PAYE or IBR. You can apply for this change through the Department of Education.

If you’re not eligible for PAYE or IBR now, but think you might be close, consider a few strategies to reduce your adjusted gross income to become eligible:

- Has your income decreased since your last tax return on file? If so, use alternative documentation of income such as a paystub or an offer letter to base your payment off of versus the tax return.

- File taxes separately from your spouse to exclude spousal income from your payment calculation.

- Reduce your adjusted gross income by contributing more to your pre-tax or tax-deferred savings vehicles, such as: 401(k), 403(b), TSP, 457, IRA, SIMPLE IRA, SEP-IRA, or HSA.

Maximizing the efficiency of your student loan repayment plan

Navigating the best way to take advantage of the partial financial hardship is complicated. Luckily, we're experts in slaying complex student loan situations.

We've helped 5,382+ clients take on over $1.34 billion of student debt optimize their repayment strategy. We live and breathe student loans!

Our student loan consultants would love to make a custom plan for you so you don't have to go it alone anymore.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).