Income-driven repayment (IDR) plans help federal student loan borrowers avoid unmanageable payments. Generally, as your income increases, so does your monthly payment. However, IDR plans like Income-Based Repayment (IBR) and Pay As You Earn (PAYE) offer a safeguard by capping payments at a level comparable to the 10-Year Standard Repayment Plan.

This is now significantly easier under new legislative changes as of July 2025 with the OBBB Act, which allows any borrower who is otherwise eligible for IBR to simply apply and receive a capped payment regardless of income.

Having a maximum payment cap is especially valuable for borrowers who expect a rapid increase in income, such as doctors and dentists. Keep reading to learn how to calculate your payment cap on IBR and PAYE.

Which IDR plans have a payment cap?

Borrowers with federal student loans can choose from four income-driven repayment plans. But only IBR and PAYE have capped payments, which used to require a “partial financial hardship” to qualify. This used to mean that your IDR payment can’t exceed the calculated payment under a 10-Year Standard Repayment Plan to be eligible.

After enrolling in IBR or PAYE, your monthly payments will continue to increase with your income until you hit your payment cap. Then, you can ride out monthly payments at that maximum payment cap — regardless of how much money you make.

That said, the new IBR legislation means you could be on a different repayment plan or no IDR plan at all and still apply and qualify for IBR with a capped payment, even if you make $1 million a year.

Here's how these different plans compare.

| IDR Plan | Capped Payments | Payment | Forgiveness Timeline |

|---|---|---|---|

| IBR plan | Yes | 10% to 15% of discretionary income | 20 to 25 years |

| PAYE plan | Yes | 10% of discretionary income | 20 years |

| SAVE plan (now eliminated) | No | 5% to 10% of discretionary income | 20 or 25 years |

| ICR plan | Yes | 20% (of income above 100% of poverty line) | 25 years |

| RAP Plan | No | $10 a mo to 10% (of AGI less $50 per month per dependent) | 30 years |

IBR and PAYE payment caps allow borrowers to still get loan forgiveness, such as Public Service Loan Forgiveness (PSLF), even if they have a super high income. It acts as a payment ceiling, allowing for more affordable student loan payments.

How does the payment cap work for IBR and PAYE?

While already enrolled in the IBR and PAYE plans, your payment can’t exceed what you’d pay under the 10-Year Standard Repayment Plan. The Department of Education determines your 10-Year Standard payment amount using the greater of either:

- Your loan balance when entering repayment for the first time (ever or when you consolidated).

- Your loan balance when you initially applied for income-driven repayment.

For example, if you have several forbearance periods early on and finally apply for income-driven repayment after accruing a ton of interest, your payment cap is going to be higher because your loan balance grew. But if you had applied for an IDR plan immediately after graduation, your original loan balance would be used when calculating your IBR or PAYE payment cap.

You can calculate your IBR or PAYE payment cap in a few ways:

- Check with your loan servicer. Ask what your maximum payment could be on PAYE or IBR. You can also ask what your 10-Year Standard Repayment monthly payment would be.

- Estimate the payment amount yourself. Let’s say you applied for income-driven repayment five years ago. You’ll need to look at your loan balance from that same time period. Then, you’ll calculate what it would have taken to pay that balance off amortized over 10 years.

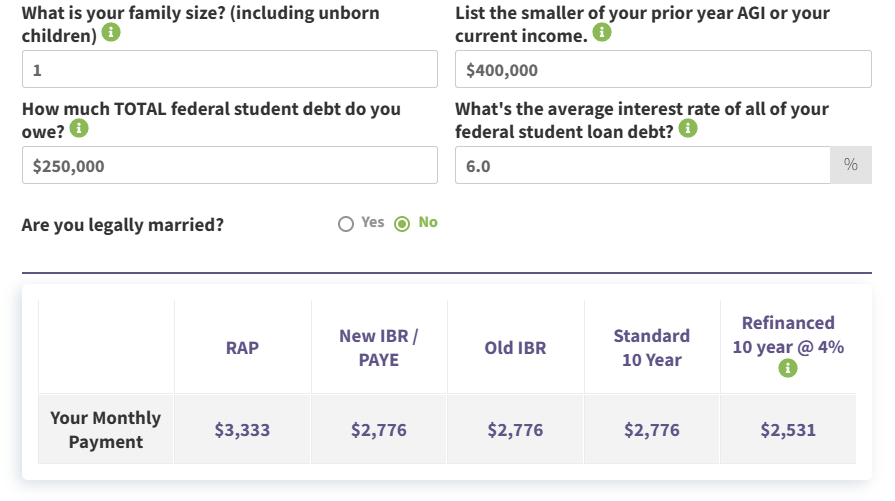

- Use our income-based repayment calculator. Compare existing IDR plans and determine your payment cap for IBR and PAYE based on the projected 10-Year Standard payment. The example below shows that a single borrower with $250,000 in federal debt has a payment cap of $2,776. They can rest assured that their IBR or PAYE payment won’t increase beyond that even if they start earning $400,000 or more.

Can I be kicked off IBR or PAYE if my income exceeds the payment cap?

Thankfully, no. Once you’re on IBR or PAYE, your loan servicer can’t kick you off based on your income. But you might receive some conflicting communication that might make you think you’re no longer eligible.

This communication confusion will likely decrease in the coming years, as the One Big Beautiful Bill Act now allows any borrower with loans exclusively taken out before July 2026 to access the IBR plan with a payment cap equal to the Standard 10 year plan.

Let’s say you’re earning a lot more money but qualify for IBR or PAYE. You go to recertify your income, and your monthly payment would be above that 10-Year Standard Repayment payment cap. You now can just apply for IBR directly. That said, it might take several more months for the online systems to be updated.

If you ever get told you no longer qualify for IBR because you make too much money, call your servicer and let them know that is no longer correct under new legislation. You’ll continue making payments based on your payment cap until you reach loan forgiveness status — either with PSLF or long-term IDR forgiveness. Note that in some cases, you could potentially pay off your balance before being eligible for forgiveness.

Common borrower question: Can’t I just switch back to the 10-Year Standard Repayment Plan?

Our consultant team often has borrowers ask if they can just switch back over to the 10-Year Standard Repayment Plan once their income increases. Technically, you can. But it’s not straightforward in the way you think. Here’s why.

Borrowers with consolidated loans

Once you consolidate, the Standard Repayment Plan extends out according to the balance size. This means your Direct Consolidation Loan could extend out up to 30 years, depending on your loan balance. For example, if your student loan balance is over $60,000, the amortized Standard Repayment Plan becomes 30 years instead of 10 years.

How does this play out for borrowers with consolidated loans?

Let’s say you’re a medical resident making $65,000 right now, so it might make sense to be on an IDR plan. But your payment is going to be much higher in several years when you’re earning your full attending salary of $300,000.

Some borrowers in this situation assume they can just switch back to the 10-Year Standard Repayment Plan to avoid higher monthly payments but still be eligible for PSLF. Unfortunately, that’s just not possible. Yes, you can technically apply for the Standard Repayment Plan. But your payment won’t be based on 10 years — which is what makes a Standard 10-Year plan eligible for PSLF. Your payment is going to be based on the 30-year amortized schedule because you consolidated your loans.

Therefore, you’re better off staying on IBR or PAYE and using the payment cap to your advantage.

Borrowers with unconsolidated loans seeking PSLF

If you’ve never consolidated your student loans and expect significantly higher income in the future, switching to the 10-Year Standard Repayment Plan at a later date isn’t going to work either.

When you apply for the 10-Year Standard Repayment Plan, the Department of Education will take into account any time already spent in repayment. If you’ve been on an IDR plan for five years and you decide to switch over, they’re going to treat your loans as if you only have five years left of the Standard Repayment because you’ve already paid for five. Therefore, they will amortize your remaining balance and calculate your payments based on paying your loans off in the final five years of that 10-year timeline.

In this scenario, you wouldn’t be able to take advantage of PSLF loan forgiveness. Instead, you’re going to end up paying off your full balance because the system is set up to do the math to pay it off within what’s left of the 10 years. Again, utilizing the IBR or PAYE payment cap is your best path forward for PSLF if you expect to make a high income.

Potential payment cap mishap for borrowers who consolidated

Let’s say you’ve been on an IDR plan since 2012, but you consolidated your loans in 2018. The new Direct Consolidation Loan is essentially a brand new loan, so it wipes the slate clean. Therefore, your payment cap is going to be based on the new consolidation loan balance from when you entered IDR repayment again in 2018 — not the payment cap from 2012 before you consolidated.

That's why it's easier to just apply for IBR right away and get a capped payment even if you make a lot of money. The new OBBB Act allows this, but it didn't in the past.

Our team of student loan experts have consulted on over $2.6 billion of student debt and are available to help in these situations where you need to understand your new options post-legislative changes. Get in touch for a custom repayment plan that factors in possible student loan changes down the pipeline to give you peace of mind.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).