Students and their families across the country receive their financial aid packages ahead of the upcoming school year. Understanding its fine print can help you make an informed decision about finding the best college fit and how much it’ll ultimately cost.

Unfortunately, many financial aid awards aren’t only very confusing, but also fall short of what families were expecting. However, you can appeal your award and ask for more money.

A financial aid appeal, also called a professional judgment review, is a formal request by a student or their family for additional financial aid. But beware — it’s not an easy process and not always successful. Here’s what to know about appealing your financial aid award, and the process involved.

Best reasons for appealing financial aid awards

How do you know when submitting an appeal letter might be appropriate? Below are a few scenarios to help answer this question.

Error on financial aid application

If you entered incorrect information when submitting your FAFSA, you could submit an appeal to correct the error (e.g., misreported financial information or a change in dependency status).

Special circumstances

If you experienced a change in income or an increase in personal expenses, you might be able to appeal your aid package. The most common special circumstances include:

- Job loss or reduction of income.

- Fuctuation of income (i.e., small business owners).

- Divorce or separation.

- Death or disability of a parent.

- Unreimbursed medical expenses.

- Support of an elderly parent.

- Damage due to a natural disaster.

- A one-time increase in a family’s income (i.e., premature IRA withdrawal, severance pay, etc.).

Competitive offers

If the student has received acceptance offers with larger aid packages, you can reach out to the schools to see if it’ll offer a match. It’s key that you leverage an aid package from a school that’s comparable to the one you’re requesting more funds from. However, check the school’s website and/or ask if this would matter, as many schools explicitly state that they won’t review these types of appeals.

Exceptional merit

If the student received awards or recognition, has increased their GPA and/or test scores or has added more extracurricular activities since submitting the admissions application, it could result in more aid via an appeal. The school might now view the student as a potentially excellent addition to its campus and have a new reason to offer an enhanced incentive to offer more aid.

How to appeal your financial aid award

Once you’ve assessed your circumstances and are certain you want to appeal your award, start the appeals process as soon as possible. Here is how to get started with your financial aid appeal:

- Ask your school about its appeals process. Every school has a different approach to appeals. Some require a mailed or emailed letter, while others have a formal appeals application through the school's portal or website. Also, it’s best to talk to someone in person (e.g., a financial aid or admissions counselor) who might be willing to go to bat for you rather than simply submitting the appeal.

- Strategize who should write the letter. A school might have explicit instructions regarding who should submit the appeal—the parent, the student or both. When appealing merit aid, the student should typically make the appeal. When submitting a special circumstance appeal (e.g., a change in financial situation), generally speaking, a parent should make the appeal; in some cases, both the parent and student should submit an appeal.

- Include the student’s information. In your letter, include specific details about the student, like their student ID or reference number, if applicable.

- Be direct, concise and to the point. Limit it to one page, which will help the reader. Clearly state the need for more aid and explain the circumstances.

- Provide adequate supporting documentation. Provide proof of your reasons for the appeal, especially if the letter references specific financial amounts. If income changes, show the supporting documentation for the change, like a recent tax return.

What to expect after submitting an appeal

Keep in mind that appealing for additional dollars isn’t a sure thing. It all depends on your school, their applicants that year, and the type of appeal you’re submitting (i.e., special circumstances, merit, etc.).

For example, elite colleges and universities typically offer no merit aid because they don’t have to — wealthy or rich parents are willing to pay full price for brand-name schools. Public schools tend to have less money to offer, and thus successful appeals are rare unless there’s an extreme financial hardship. Also, if schools have a large applicant pool, it might be less inclined to give more aid because there are plenty of students who would gladly pay with no aid. But, you can still ask if you have a need.

When it comes to how soon you’ll receive a response, some schools respond quickly, within 24 to 48 hours; others might not give you a decision until September. However, most colleges are somewhere in the middle, which is generally 4 to 6 weeks. The typical appeal results in a $3,000 to $5,000 additional award.

Examples of financial aid appeal letters

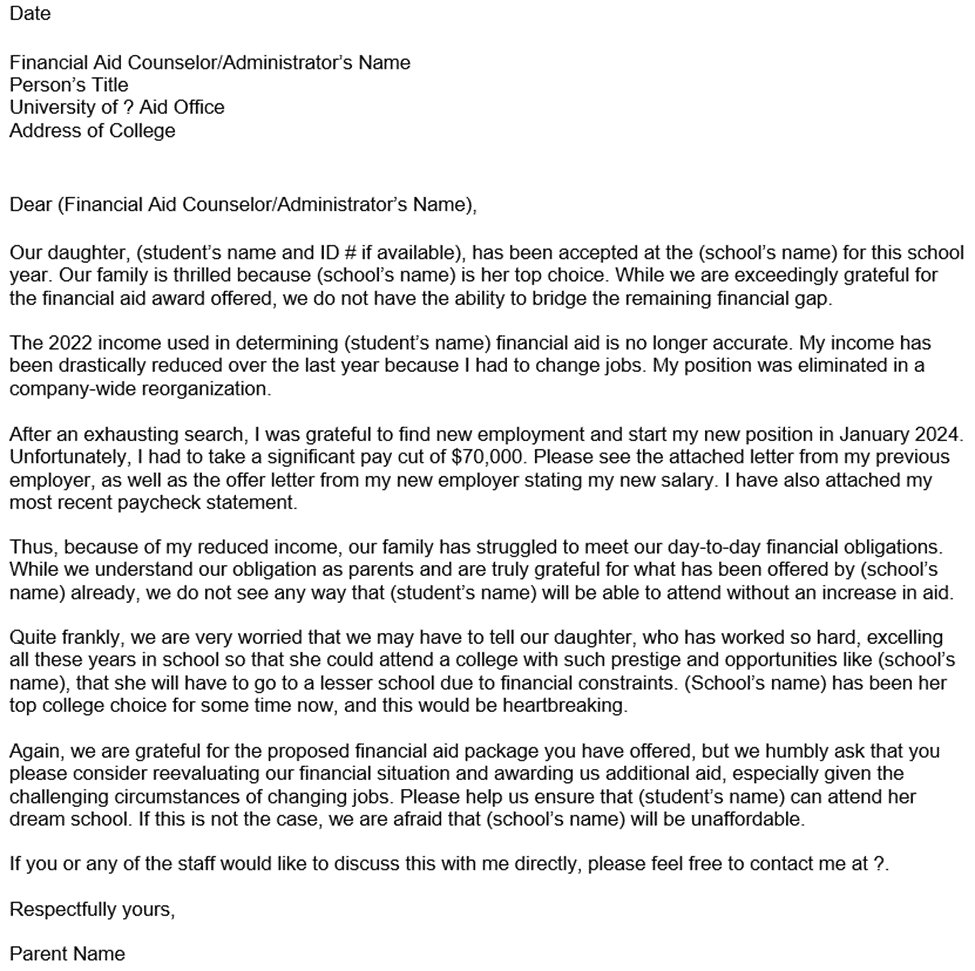

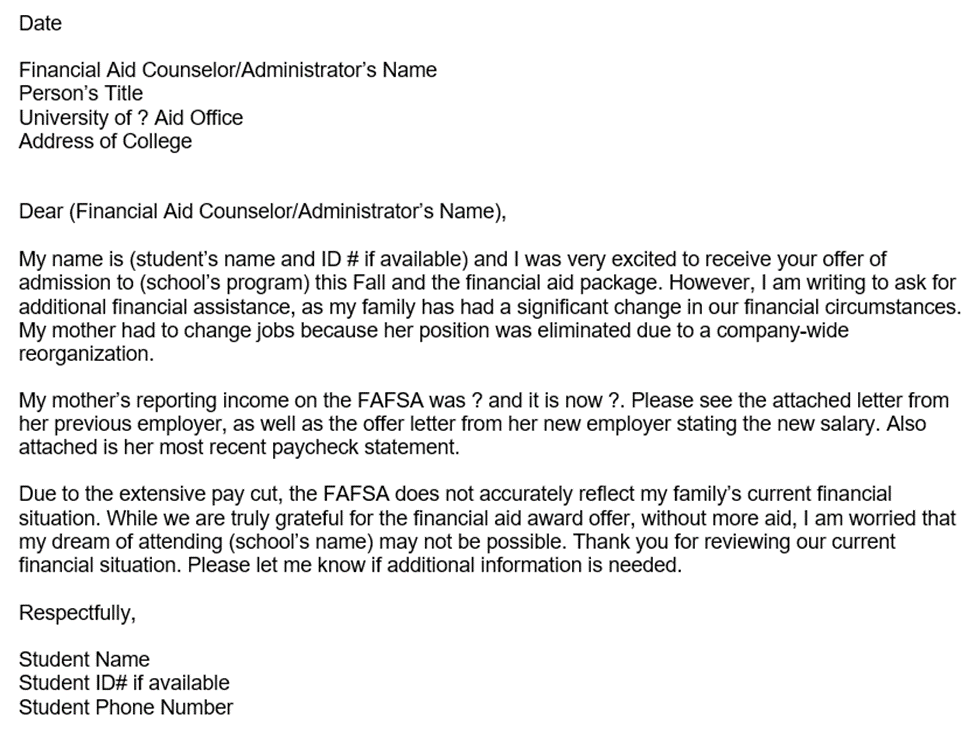

One example scenario when an appeal letter might be worth submitting is if a significant income change occurred.

Let’s say a student is an incoming first-year student in 2024. Financial aid applications request tax data from the prior-prior year; in this case, that’s their 2022 tax return. During the 2022 tax year, their parents filed as married, filing jointly.

One parent has changed jobs since 2022, which resulted in a $70,000 pay cut. Their health insurance is also more expensive than at their previous job, further reducing the parent’s net pay.

The family’s EFC was $42,406. If the school accepts the full impact of the reduced income, it could result in an EFC change of nearly $31,000, which could significantly change the student’s financial aid award.

NOTE: To make the application process easier for students and their families, Congress passed the FAFSA Simplification Act, which included major changes to the FAFSA. One such change replaced the term Expected Family Contribution (EFC) to the Student Aid Index (SAI). These changes resulted in a FAFSA release date delay from its usual October 1 release. This year, it was released in December. The set back caused ripple effects, including delayed distributions of financial aid awards. The sample financial aid awards and case study that follows uses the term EFC, as it's from the 2023-24 school year. However, these are still useful and relevant tips that can help you navigate the financial aid appeal process.

Below are examples of how a parent vs. a student might phrase the appeal letter in this situation.

Sample financial aid appeal letter, written by the parent

Sample financial aid appeal letter, written by the student

Top financial aid appeal tips

Below are a few strategies to heed when appealing your financial aid package.

Provide evidence

This tip bears repeating, especially if you’re submitting a special circumstance appeal. Be prepared to provide evidence or documentation to support your appeal request.

Clearly explain why you need the money. Common documentation includes tax returns, a letter from an employer (i.e., stating a reduction in hours and/or pay), a W-2, layoff notices, medical/dental bills, letters from those who are familiar with the family’s situation (i.e., divorce attorney, doctor, social worker).

Also, make copies of all documents before submitting them to the school. Don’t send originals, as they likely won’t be returned. If you’re submitting an appeal on the basis of merit, attach transcripts, merit awards or any information that supports your claim.

Don’t negotiate

When appealing your award, don’t antagonize those reviewing your letter by using the word “negotiate.” Colleges don’t like the word “negotiate” because it sounds like bargaining with them like you do when you shop for a car.

Instead, use the word “reconsider.” Understand that while financial aid and admissions counselors must follow a process, some might have the power to dispense better financial aid awards than others. You don’t want to come on too strong.

Don’t submit a deposit

Typically, the traditional deadline for students and their families to commit to a school is May 1. However, given the delay in the roll out of the FAFSA this year, many schools have extended that deadline.

When committing to a school, it requires a deposit to essentially save your seat that ranges from $100 to $500 on average. If you commit and submit your deposit early, colleges don’t have much incentive to work with you because they already have your money.

It’s best to hold off on paying the deposit until the final cost is determined unless it’s your first choice school and you’re planning to attend despite an unsuccessful appeal.

Ask for a specific dollar amount

Some experts recommend refraining from asking for a specific amount of money, as doing so might backfire. Others recommend the opposite — if there is a specific amount of money that you need, ask for it.

A general rule of thumb is if you know there’s a specific amount that you need for the school to be a viable option, then ask for the specific amount. Otherwise, if you’re simply asking for an increase, but will keep the school in the running regardless of the appeal decision, don’t ask for a specific amount.

Be polite

Express gratitude and thanks for the aid that you have already been offered. Also, conclude the letter by thanking the school for its consideration of your appeal.

Be proactive, follow up

Call the school within a week or so of your submission to confirm receipt and ask if any additional information is needed.

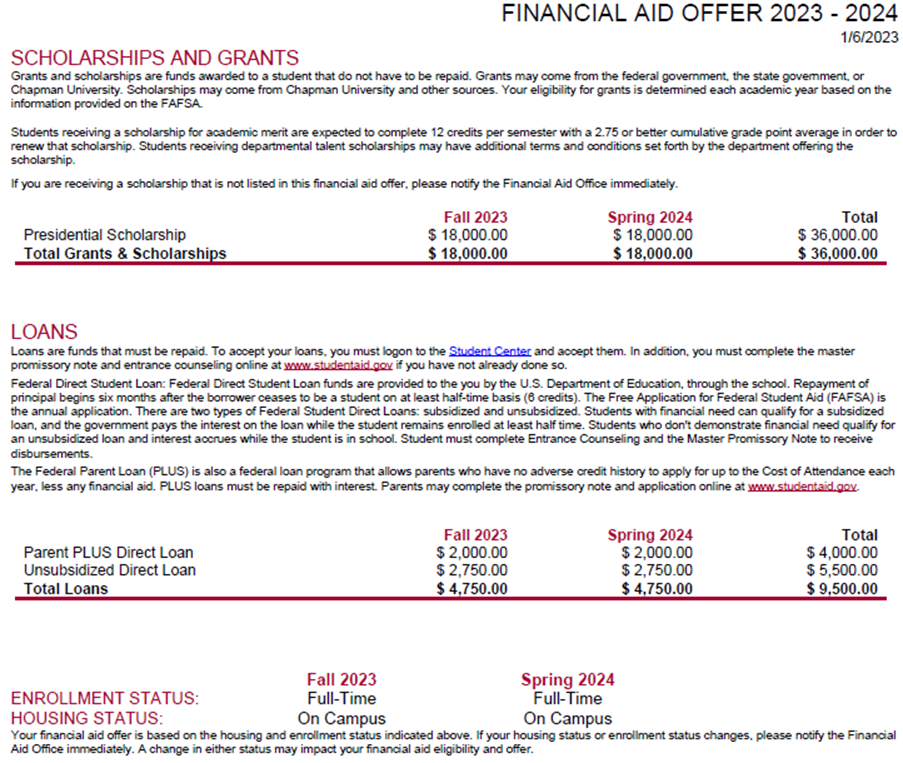

Case study: A financial aid package that’s worth appealing

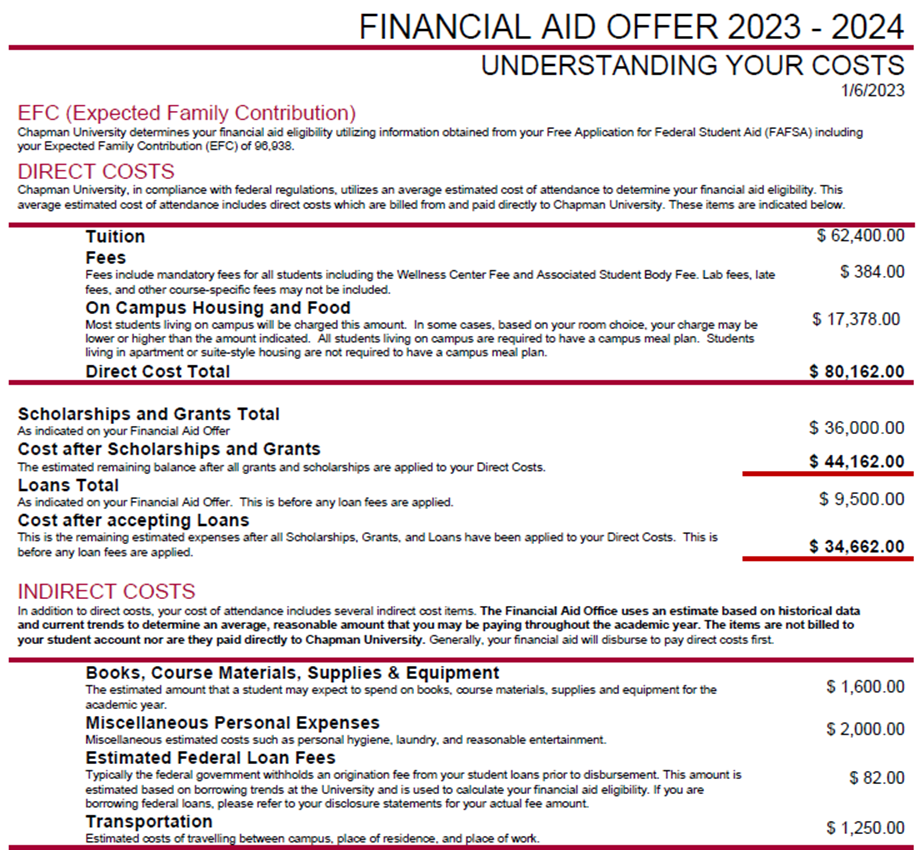

Below is an example award letter from a university on the west coast. The letter provides the grants, scholarships and loan information. Although the full cost of attendance (COA) and net price aren’t explicitly stated, all of these details are provided. The student aid index (SAI) — previously the Expected Family Contribution (EFC) — measures the family’s financial ability to pay for college. It's also shown, albeit in small print.

One detail to note is that the unsubsidized Direct and PLUS Loans are used to reduce the family’s financial obligation when, in fact, they don’t. That type of aid must be repaid with interest plus an additional origination or processing fee. When omitting the $9,500 for loans, the net price is actually $44,162.

The family’s SAI/EFC ($96,938) also exceeds the university’s COA, which is extremely high, given that this family has twins. As a result, the family appealed the financial aid offer.

The appeal was successful, and the school offered two additional grant awards, plus a subsidized Direct Loan. The resulting aid, after appealing the first package, brought their “net price” down to just over $22,000.

Alternative aid options if your appeal is rejected

If you’ve submitted an appeal but still need more money for college, below are additional options to explore.

- Private loans. This student aid is issued by a bank or other financial institution in the student’s name but often requires a creditworthy co-signer. If you are in need of a private loan, be sure to shop around and find those that are fixed rate and have flexible repayment options. Private local scholarships

- Third-party scholarships. Private scholarships are awards offered by foundations, charities, companies and civic groups. They represent the smallest source of college funding but offer a better chance at funding since local scholarships aren’t typically advertised on big college aid databases. NOTE: Private scholarship awards may decrease the amount of financial aid awarded by the school.

- Work-study. Work-study is a federal program that provides students with a part-time job while enrolled in school. The money earned doesn’t have to be repaid. However, not all students qualify for federal work-study.

- Part-time job.Income from a part-time job while in school can also help boost income and pay for college expenses. In fact, working full-time during the summer months can help pay for next year’s expenses.

- Co-op or internships. Cooperative education (co-ops) and internships are experiences that allow students to increase their knowledge and gain work experience in their chosen career path. During these programs, students can also earn compensation to help with school expenses. An internship is usually a one-time work assignment, during the summer or an academic semester. They can be part-time or full-time, paid or unpaid. Co-ops are usually full-time, last for a longer duration with one employer, and the responsibilities increase as their education progresses.

Additional options to consider include taking a gap year to earn and save more money or researching regional tuition exchange programs. You might also transfer to a more affordable school and take courses at a community college over the summer. For high school students preparing for college, take advantage of advanced placement and dual-enrollment opportunities.

If your financial situation merits more aid, it’s worth an appeal

Financial aid is a crucial component of a college plan. Students and their parents are often surprised that their financial aid awards weren’t larger but never do anything about it. It’s unfortunate because many colleges are willing to offer more aid if asked.

Understand that the first offer from a college isn’t always the final offer. If you don’t get enough financial aid and think you have a case for an appeal, formulate a plan immediately. The sooner you submit an appeal, the better your chances at success.

As other students decline their offers, schools might have more aid to offer. Being proactive can potentially save you thousands of dollars. The key to your success is providing your school with the proper supporting documents in a succinct, concise and easy-to-read appeal letter.

Private student loan options for 2026

| Lender Name | Lender | Offer | Learn more |

|---|---|---|---|

| SoFi |

|

$300 Cashback1

Bonus from Student Loan Planner®, not SoFi®

|

Fixed 2.45 - 16.73% APR

Variable 4.39 - 16.73% APR

|

| Sallie Mae |

|

$0 Cashback2

One of the top private student loan lenders by volume in the U.S.

|

Fixed 2.19 - 17.64% APR

Variable 3.75 - 17.14% APR

|

| Earnest |

|

$300 Cashback3

Bonus from Student Loan Planner®, not Earnest

|

Fixed 2.19 - 16.24% APR

Variable 4.74 - 16.60% APR

|

| Ascent |

|

$300 Cashback4

Bonus from Student Loan Planner®, not Ascent

|

Fixed 2.19 - 17.51% APR

Variable 3.60 - 16.51% APR

|

| Credible |

|

$300 Cashback5

Bonus from Student Loan Planner®, not Credible

|

Fixed 2.29% - 17.99% APR

Variable 3.50% - 17.99% APR

|