Having the right tax documentation can sometimes be the difference between owing Uncle Sam or getting a refund. Let’s look at the most important student loan tax documents you need when filing taxes. Plus, we’ll show you how to use them to lower your student loan payments.

Tax documents cheat sheet for my student loans

Tax forms have valuable information that let you claim certain tax deductions and credits to save you money. When it comes to student loan tax documents, you’ll find details related to how much interest you’ve paid on student debt, how much you’ve paid toward higher education expenses and how much student loan forgiveness you’ve received — all of which can be used to lower your tax bill.

Here’s a quick reference guide for which student loan tax documents you might need depending on whether you’re in repayment or still in school.

| Scenario | Tax form |

|---|---|

| You’re in repayment | Form 1098-E |

| You’re still in school | Form 1098-T |

| You’re paying on interest while in school | Form 1098-E and Form 1098-T |

| You received loan forgiveness (or other debt cancelation) | Form 1099-C |

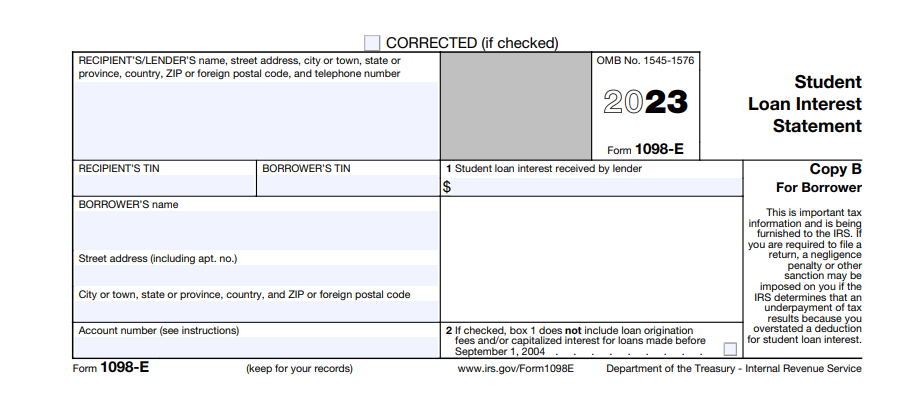

For borrowers repaying student loans: Form 1098-E (Student Loan Interest Statement)

If you’re currently paying back your federal or private student loans, you should receive IRS Form 1098-E from your student loan servicer if you paid at least $600 of interest for the year. This is the student loan tax document used to claim the student loan interest deduction, which allows you to deduct up to $2,500 in paid interest (depending on your filing status and adjusted gross income).

Box 1 of Form 1098-E will show the amount of interest you paid on student debt throughout the year, which is pretty straightforward. But we often get asked if borrowers can claim the deduction if they consolidated or refinanced their student loans. And the answer is yes.

You can claim the student loan interest deduction based on the amount reported on your 1098-E tax form, regardless of whether that money came directly out of your pocket or if it was paid during the consolidation or refinancing process. Any caveats to those scenarios should be caught by the checkbox in Box 2 that deals with loan origination fees and capitalized interest for loans before September 1, 2004.

Note if you don’t receive a mailed 1098-E form, you can download a copy from your loan servicer’s website.

Limitations to the student loan interest deduction

You won’t be able to claim the student loan interest deduction if you’re married filing separately.

Additionally, if your modified adjusted gross income (MAGI) is between $75,000 and $90,000 for single or head of household or $155,000 to $185,000 for married filing jointly, then your student loan interest deduction will be gradually phased out. If your MAGI is above those limits, you won’t be able to claim the student loan interest deduction.

Tip: The IRS has a useful tool for determining whether you can claim the student loan interest deduction using its Interactive Tax Assistant.

Is financial planning with SLP Wealth right for you?

Looking for student loan aware financial planning custom tailored for professionals like you? Check out the discounts below for becoming a client of SLP Wealth (our SEC Registered Investment Advisory firm).

SLP Wealth, LLC (“SLP Wealth”) is a registered investment adviser registered with the United States Securities and Exchange Commission with headquarters in Durham, NC.

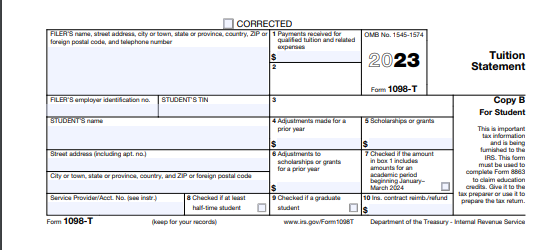

For borrowers currently in school: Form 1098-T (Tuition Statement)

If you’re still in graduate school or taking undergraduate classes, you should receive IRS Form 1098-T from your college or university. This student loan tax document reports any paid qualified tuition and education expenses and is used to claim certain education tax credits.

Box 1 of the 1098-T will show exactly how much was paid to a qualified institution for tuition, fees and other related education expenses — even if they were paid for with student loans.

Box 5 will account for any scholarships or grants that were paid directly to the institution for school expenses. If Box 5 is less than Box 1, you can use the difference to get an offsetting tax credit for your out-of-pocket education expenses.

Available education tax credits

Unfortunately, the tuition deduction is no longer available. But you can still potentially take advantage of the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC). The main perks of these tax credits include:

- American Opportunity Tax Credit:Able to get a maximum annual credit of $2,500 per eligible student for the first four years of higher education, including 100% of the first $2,000 of qualified expenses and 25% of the next $2,000. This tax credit is partially refundable.

- Lifetime Learning Credit: Able to claim up to $2,000 for qualified expenses for undergraduate, graduate or professional degree courses. This tax credit doesn’t have a limit on the number of years you can claim it, and it isn’t refundable.

Note that both education tax credits have income limits and other eligibility requirements to be aware of, and each functions differently.

For example, the American Opportunity Tax Credit is more generous than the Lifetime Learning Credit. But it can only be claimed for the first four years of post-secondary education. Therefore, it’s typically only claimed for undergraduates.

Because of this, it can be a bit of a red flag for the IRS if the checkbox in Box 9 of your 1098-T is marked for graduate school and you try to claim the AOTC. That said, if you finished undergrad early, your first year of grad school could count as your fourth year of post-secondary. In which case, the American Opportunity Tax Credit could still be on the table.

Should I claim the American Opportunity Tax Credit or the Lifetime Learning Credit?

You can’t claim both the AOTC and LLC for the same student or the same qualified expenses in the same year — aka there’s no double dipping.

It’s best to prioritize claiming the American Opportunity Tax Credit for the first four years of post-secondary to receive a larger tax benefit. If you’re still getting a 1098-T after that timeframe, then move on to the Lifetime Learning Credit.

Education tax credits for parents

If you’re a Parent PLUS borrower or have children in higher education, you can claim these education tax credits as long as the student is listed as a dependent on your tax return.

Keep in mind that you’re able to claim these tax credits per individual dependent, which can add up quickly if you have multiple children in school at the same time.

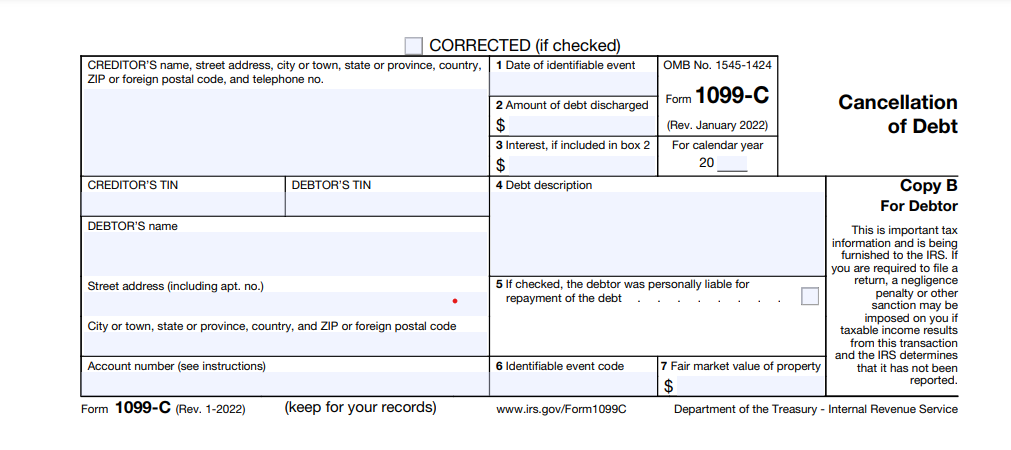

For anyone who received forgiveness: Form 1099-C (Cancelation of Debt)

Another student loan tax document that can make a big difference in your tax bill is IRS Form 1099-C, which you should receive if you had more than $600 of debt canceled from any lender.

But borrowers need to pay extra attention to this form if they receive student loan forgiveness.

Public Service Loan Forgiveness (PSLF) is always tax-free. But thanks to the American Rescue Plan, other forms of student loan forgiveness are tax-free through the end of 2025. This might include scenarios like:

- Your private student loans are discharged through bankruptcy.

- Your federal student loans are forgiven under an income-driven repayment (IDR) plan.

- Your federal student debt is canceled through a mass forgiveness effort in the future.

That said, this legislation is only from a federal perspective. Any canceled student loan debt might still be subject to state taxes.

Here’s where the 1099-C really comes into play in relation to being aware of student loan forgiveness at tax season…

The 1099-C form is designed to report any type of debt cancelation, not just student loans. And there’s no definitive indicator on the form relevant to student loans like you’ll find with the 1098-E and 1098-T. Box 4 does have an area available for debt description. But these forms are often left blank.

So, this can become a major issue for borrowers getting their taxes prepared between now and into early 2026 (for tax year 2025). If your tax preparer doesn’t know to ask if the debt cancellation was for student loan forgiveness, you could miss out on huge tax savings.

How to lower IDR payments using your student loan tax documents

There are a variety of strategies you can use to lower your federal student loan payments, some of which involve using tax documentation to your advantage.

Using alternative income documentation vs. automatic recertification

Whether you’re enrolling in an income-driven repayment plan for the first time or recertifying your income on StudentAid.gov, you’ll be asked to provide income information. This can be done in one of two ways:

- You can authorize the IRS Data Retrieval Tool to transfer your federal tax information into the application.

- You can provide alternative income documentation.

Giving authorization to retrieve federal tax information is going to be the easiest way to recertify your income. By giving approval to do so, the U.S. Department of Education will automatically recalculate your eligibility and monthly payment amount using your federal tax return information each year. But that doesn’t necessarily mean it’s the most advantageous route for your student loans.

You also have the option to use an acceptable form of alternative income documentation. This might include providing recent pay stubs, submitting a letter from your employer certifying your gross pay or signing a statement explaining your income.

If your adjusted gross income is lower than your most recent tax return or you’ve been advised to provide alternative documentation for other reasons (e.g., you live in a community property state and don’t earn as much as your spouse), then you’ll benefit more from declining to automatically access your federal income information.

What happens after I give consent to import federal financial information for my IDR application?

Once you consent to transfer your IRS financial information, this authorization will stay remain active for future recertification years. When that happens, the Department of Education will automatically import your financial data into your recertification each year.

However, you have the option to revoke this consent at any time. If revoked, you must reauthorize before your IDR anniversary date or be prepared to submit alternative income documentation.

Certifying income as soon as you graduate

You can consolidate your loans and choose an income-driven plan immediately following graduation at a time when your income is still low.

In this situation, the new SAVE plan is generally going to be your best bet due its generous interest subsidies and payment calculation that is based on 5% to 10% of discretionary income.

However, there are some exceptions where PAYE could be more beneficial. For example, if you’re projected to completely pay off your loans on a 25-year plan, you might benefit more from PAYE where you’ll receive loan forgiveness after 20 years. That said, new enrollment for PAYE will be blocked after July 2024.

Filing taxes separately

You can get a lower IDR payment in most cases by filing taxes separately from your spouse. However, it could have other consequences, such as disqualifying you from certain tax credits and preventing you from receiving Affordable Care Act (ACA) subsidies.

Related: How to Decide When To Use Married Filing Separately

Delaying your federal tax return filing

If you’re already in repayment and your IDR plan anniversary date is between April and October, you can strategically file an extension for your federal tax return to get a more favorable student loan payment. Filing an extension forces the Department of Education to use income information from the previous year’s tax return for IDR recertification.

For example, if you delay filing for the 2023 tax year, the Department of Education will use your 2022 income information instead to calculate your 2024 student loan payments.

Timing your recertification for the most benefit

You can strategically time recertification (or switching IDR plans) to create a built-in delay where your student loans don’t necessarily reflect your current income level.

January and February can serve as a sweet spot for recertifying your income since it’s almost guaranteed that you haven’t filed your tax return yet. So, it creates a good lag where the Department of Education will have to reach back almost a full year for income information.

Recertifying when your income drops

You can recertify your income early if it’ll ultimately benefit you. You don’t have to wait for your anniversary date each year. So, if your income drops, you’ll want to recertify as soon as possible to get a lower student loan payment. The best part is that it essentially locks in that lower student loan payment for the next 12 months, even if your income increases before your next recertification date.

Consider recertifying immediately if you:

- Lose your job or cut back on hours.

- Go on parental leave for a birth or adopted child.

- Experience a disabling condition and begin collecting disability income that’s less than your regular income.

You should also recertify if your family size increases as it factors into the discretionary income calculation. You can update your family size as soon as you learn of a pregnancy.

Adjusting pre-tax contributions to reduce AGI

IDR payments are determined based on a percentage of your discretionary income, which factors in your adjusted gross income and your family size. Therefore, lowering your AGI will also reduce your student loan payments.

Two effective ways to reduce your AGI is by increasing contributions to:

- Pre-tax retirement accounts (e.g., Traditional IRA, 401(k), 403(b), 457).

- Your Health Savings Account (HSA) if you have a high deductible health plan (HDHP).

Note if you make contributions through an employer-sponsored HSA account, those contributions should be captured within your W-2. But if you’re making HSA contributions outside of an employer-sponsored account or are making after-tax contributions on your own, you can use Form 5498-SA to reclaim those contributions on your taxes.

Be aware that this form has a tendency to arrive after the tax filing deadline. But you should be able to use your online account to look up contribution amounts if needed.

Simplifying the chaos of student loan tax documents

Smart tax planning includes factoring in student loan repayment strategies and ensuring you have all tax documents lined up to maximize tax deductions and credits.

Our team of expert financial planners can save you time, money and a whole lot of headache by streamlining your taxes and student loan repayment. Join SLP Wealth today.

Get the best discounts for financial planning with SLP Wealth

See what discounts you could get by filling out the form below.

SLP Wealth, LLC (“SLP Wealth”) is a registered investment adviser registered with the United States Securities and Exchange Commission with headquarters in Durham, NC.